Accessing Capital: A Comprehensive Guide to Securing a Business Loan

For entrepreneurs and business owners looking to fuel their growth, securing a business loan can be a pivotal step. However, navigating the lending landscape can be daunting, and it’s crucial to understand the requirements and criteria involved before embarking on the application process. This comprehensive guide will provide you with a thorough understanding of what it takes to qualify for a business loan, empowering you to make informed decisions and increase your chances of success.

Qualifying for a Business Loan

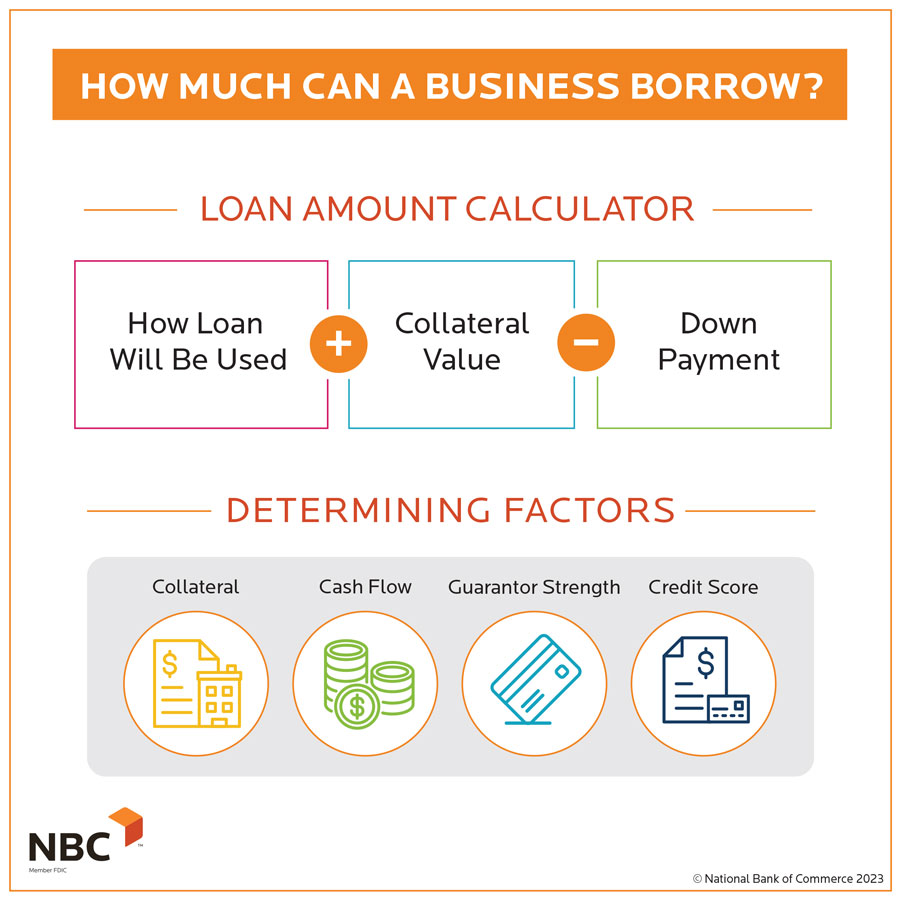

Before you can secure funding, lenders will scrutinize your business’s financial health, stability, and potential. They want to assess if you possess the qualities that indicate a low risk of default. Here are the key factors that influence loan eligibility:

Credit History and Score

Your personal and business credit histories play a significant role in the lender’s decision-making process. A strong credit score and a spotless track record indicate that you have responsibly managed your finances in the past, making you a more attractive borrower. Lenders will review your credit reports to assess your creditworthiness and determine the interest rates and loan terms you qualify for.

Business Plan and Financial Projections

Your business plan is the roadmap that outlines your company’s goals, strategies, and financial projections. A well-crafted business plan demonstrates to lenders that you have a clear understanding of your industry, market, and competitive landscape. It also provides a projection of your future revenue and expenses, enabling lenders to evaluate the viability of your business and its potential for repayment.

Collateral and Personal Guarantees

In some cases, lenders may require collateral to secure the loan, such as real estate or equipment. This provides them with an additional layer of protection if you default on the loan. Additionally, they may request personal guarantees, which bind you legally to repay the loan personally if your business cannot meet its obligations.

Ownership Structure and Management Team

Lenders will also examine the ownership structure of your business and the experience and qualifications of your management team. They want to ensure that your business has the necessary leadership and expertise to operate successfully and repay the loan.

Industry Risk and Seasonality

The industry in which your business operates can also influence your loan eligibility. Some industries, such as technology or healthcare, are perceived as higher risk than others. Additionally, lenders will consider the seasonality of your business and its impact on your cash flow.

To Get a Business Loan: A Comprehensive Guide for Entrepreneurs

If you’re looking to take your business to the next level, obtaining a business loan is often a necessary step. With countless options available, it’s crucial to navigate the complexities to find the one that suits you best.

Types of Business Loans

The loan landscape is vast, offering a diverse range of loan types. Each has its own set of advantages and considerations, making it essential to weigh them carefully based on your unique business needs.

Short-Term Loans

Short-term loans, as their name suggests, are designed for short-term financial needs. They typically offer quick access to funds, but come with higher interest rates to compensate for the shorter repayment period. These loans can be likened to short-term lifelines, providing immediate relief without the long-term burden of high interest rates.

Long-Term Loans

In contrast, long-term loans are akin to marathons, with longer repayment periods and, consequently, lower interest rates. They are ideal for larger projects or investments that require a significant upfront capital outlay. Think of them as companions on your business’s journey, providing sustained financial support over an extended duration.

Secured Loans

Secured loans are backed by collateral, such as property or inventory, that acts as a guarantee for repayment. They often come with lower interest rates than unsecured loans, given the reduced risk for the lender. Imagine these loans as a contract, where your collateral is the stake that ensures your commitment to repaying the debt.

Unsecured Loans

Unsecured loans, on the other hand, do not require collateral. As a result, they typically carry higher interest rates to offset the increased risk taken by the lender. These loans are like trust-based relationships, where your creditworthiness and business potential become the yardstick for securing funds.

Lines of Credit

Lines of credit offer a degree of flexibility not found in traditional loans. They function like a revolving fund, allowing you to borrow as needed, up to a pre-approved limit. Consider them as a financial lifeline, providing a ready source of funds when you need them most.

How to Get a Business Loan

You may need to borrow money to start or expand your business, but how do you get a business loan?

Applying for a Business Loan

The application process for a business loan can be complex, so it’s important to be prepared before you start. You’ll need to gather financial information about your business, including your business plan, financial statements, and tax returns. You’ll also need to provide personal information, such as your credit score and Social Security number.

The lender will use this information to assess your risk as a borrower. They’ll consider your business’s financial health, your personal credit history, and your ability to repay the loan.

If you’re approved for a loan, you’ll need to sign a loan agreement. The loan agreement will specify the terms of the loan, including the interest rate, the repayment schedule, and any fees. Before you sign the loan agreement, make sure you understand all of the terms.

Getting the best interest rates on business loans

Interest rates on business loans can vary significantly, so it’s important to shop around for the best deal. You can compare interest rates from different lenders online or through a loan broker.

When you’re comparing interest rates, be sure to consider the following factors:

– The loan amount

– The loan term

– Your credit score

– The lender’s fees

You can also get quotes from multiple lenders, so that you can compare your options side-by-side.

Repaying your business loan

Once you’ve gotten a business loan, it’s important to make your payments on time and in full. If you miss a payment, you could damage your credit score and make it more difficult to get a loan in the future.

There are a few things you can do to make sure you repay your loan on time:

– Set up a payment schedule and stick to it.

– Automate your payments so that you don’t have to worry about forgetting to pay.

– Keep track of your loan balance so that you know how much you owe.

If you’re having trouble making your payments, contact your lender immediately. They may be able to work with you to create a payment plan that works for you.

How to Get a Business Loan

In today’s article, we’ll take a comprehensive look at business loans. We’ll cover the basics of how to get approved for a loan, what the different types of business loans are, and how to compare them to find the best one for you.

Getting Approved for a Business Loan

Getting approved for a business loan can be a daunting task, but it’s not impossible. There are a few key things that you need to do to increase your chances of getting approved.

-

Have a strong credit score. Lenders will look at your credit score to assess your creditworthiness. A higher credit score will give you access to better loan terms and rates.

-

Have a solid business plan. Your business plan will outline your business goals, strategies, and financial projections. Lenders will want to see that you have a clear plan for how you will use the loan proceeds.

-

Have a good track record. If you have been in business for a while, lenders will want to see that you have a good track record of success. This includes making consistent profits, being able to repay your debts, and having a good reputation in the industry.

-

Prepare a strong loan application. Your loan application is your chance to sell your business to the lender. Make sure to include all of the relevant information, such as your financial statements, business plan, and personal credit history.

Once you’ve submitted your application, you’ll need to wait for the lender to review it and make a decision. The decision process can take several weeks, so it’s important to be patient.

How to Get a Business Loan: A Comprehensive Guide

Are you an aspiring entrepreneur or a seasoned business owner in need of capital to fuel your growth? If so, securing a business loan may be the key to unlocking your financial potential. This comprehensive guide will equip you with the knowledge and strategies you need to successfully navigate the process of obtaining a business loan.

Understanding the Basics

Business loans are financial instruments that provide businesses with access to funding for various purposes, such as purchasing equipment, expanding operations, or financing research and development. These loans typically come with set repayment terms, interest rates, and collateral requirements.

Types of Business Loans

There are numerous types of business loans available, each tailored to specific business needs and circumstances. Some common types include:

– Small Business Administration (SBA) loans

– Term loans

– Lines of credit

– Invoice factoring

– Equipment financing

Qualifying for a Business Loan

Qualifying for a business loan requires meeting certain eligibility criteria set by lenders. These criteria may include:

– Strong credit history

– Stable business plan

– Sufficient cash flow

– Collateral or personal guarantees

The Application Process

Applying for a business loan involves submitting a detailed application that includes:

– Business plan

– Financial statements

– Credit history

– Personal information

Using Your Business Loan

Once you’ve been approved for a business loan, it’s crucial to use the funds wisely to maximize its impact. Consider the following tips:

– **Allocate funds strategically:** Determine how the loan proceeds will be distributed among different business functions.

– **Invest in growth initiatives:** Use the loan to finance projects or investments that have the potential to increase revenue or reduce costs.

– **Repay responsibly:** Make timely loan payments to build a positive payment history and avoid potential penalties.

Avoiding Common Pitfalls

To increase your chances of success, avoid these common pitfalls when applying for a business loan:

– **Failing to prepare:** Gather and organize all necessary financial documents and information before submitting an application.

– **Underestimating the importance of a strong credit score:** Maintain a high credit score to demonstrate your creditworthiness and qualify for better loan terms.

– **Applying for too much funding:** Request only the amount of funding you need to cover specific business expenses.

– **Ignoring the terms and conditions:** Carefully review and understand the loan agreement before signing it to avoid any surprises down the road.

Conclusion

Securing a business loan can be a transformative experience for businesses, providing access to the capital they need to thrive. By following the strategies and advice outlined in this guide, you can increase your chances of obtaining a loan and using it wisely to fuel your business’s growth and success.

Leave a Reply