Small Business Loan Approval Rate

Contrary to popular belief, getting a small business loan approved is not as difficult as you might think. In fact, the approval rate for small business loans is a healthy 65%. This means that two out of every three small businesses that apply for a loan will be approved. Of course, there are certain factors that can affect your chances of getting approved, but by understanding these factors and taking steps to improve your application, you can increase your chances of getting the funding you need to grow your business.

Factors Affecting Small Business Loan Approval Rates

There are a number of factors that can affect your small business loan approval rate, including:

### Industry

The industry you are in can have a big impact on your loan approval rate. Lenders are more likely to approve loans to businesses in industries that are considered to be low-risk, such as healthcare, education, and professional services. Businesses in high-risk industries, such as construction and manufacturing, may have a harder time getting approved for a loan.

### Credit History

Your credit history is one of the most important factors that lenders will consider when making a loan decision. Lenders want to see that you have a history of making your payments on time and that you have not borrowed more money than you can afford to repay. To improve your credit history, you should pay your bills on time, keep your credit utilization low, and avoid taking on new debt.

### Collateral

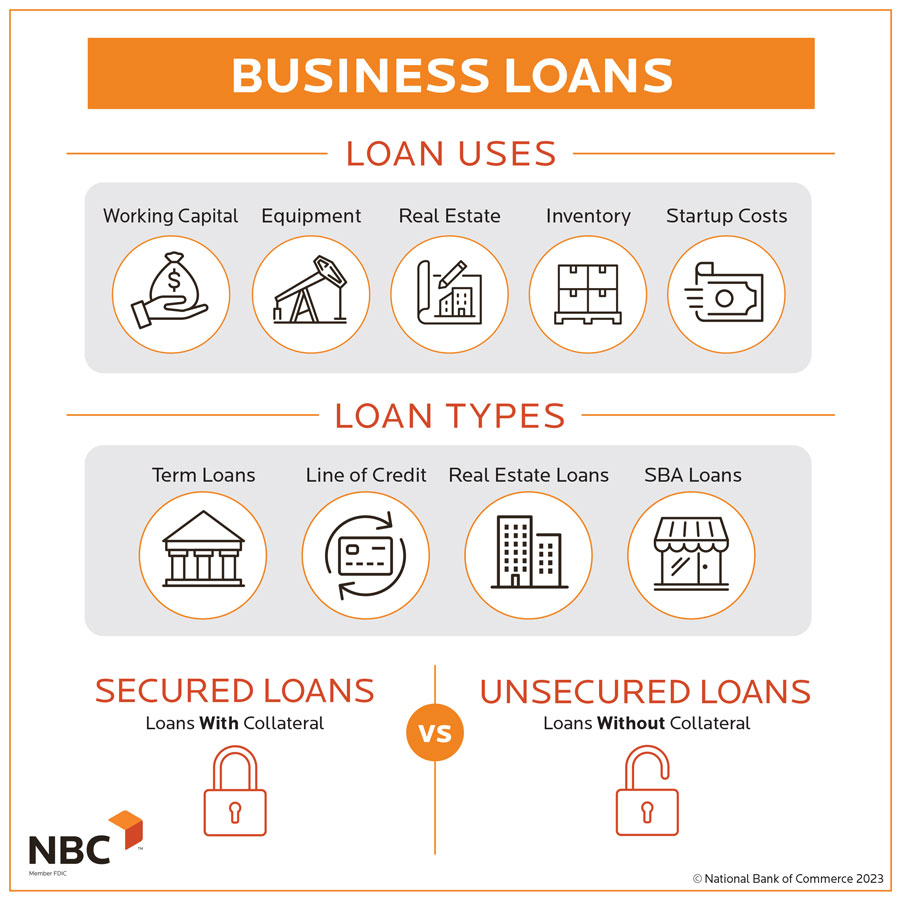

Collateral is an asset that you can offer to the lender as security for the loan. Collateral can help to improve your chances of getting approved for a loan, especially if you have a weak credit history. Common types of collateral include real estate, equipment, and inventory.

### Other Factors

In addition to the factors listed above, there are a number of other factors that can affect your small business loan approval rate, such as:

– Your business plan

– Your financial projections

– Your management team

– Your business experience

By understanding these factors and taking steps to improve your application, you can increase your chances of getting approved for a small business loan.

Small Business Loan Approval Rate

For small businesses, securing funding can be a make-or-break proposition. One key factor that can impact your chances of loan approval is your business’s credit history. As per recent industry reports, the average approval rate for small business loans hovers around 65%, making it crucial to understand how your credit score plays a role in the lending decision.

Importance of Credit History

Lenders view your credit history as a crystal ball, giving them a glimpse into your business’s financial past. It’s like a report card that shows how well you’ve handled debt in the past, and lenders use it to gauge your ability to make timely repayments on a loan.

A healthy credit history signals to lenders that you’re a responsible borrower who’s likely to repay what you owe.

On the flip side, a checkered credit history can raise red flags, making lenders hesitant to approve your loan. It’s like trying to convince your parents to lend you the keys to the car after you’ve been caught speeding a few too many times.

Your credit history isn’t just a number; it’s a narrative of your business’s financial journey. It reflects your ability to manage debt, withstand financial setbacks, and honor your commitments. By understanding the importance of credit history, you can take steps to improve your score and increase your chances of loan approval.

Small Business Loan Approval Rate: Understanding the Factors That Influence Your Chances

Securing a small business loan is crucial for entrepreneurs seeking to grow and expand their enterprises. However, the approval process can be daunting, leaving many wondering about the likelihood of success. On average, small business loan approval rates hover around 25%, making it essential to understand the factors that influence your chances of obtaining funding.

Loan Amount and Purpose

The loan amount you seek and the purpose for which you intend to use the funds play a significant role in your approval chances. Lenders are more likely to approve smaller loan requests, as they pose less risk. Additionally, loans used for working capital or inventory purchases are typically viewed more favorably than those intended for speculative ventures or risky investments.

For instance, a loan of $50,000 for purchasing new equipment has a higher probability of approval compared to a loan of $200,000 for expanding into a new market.

Business History and Creditworthiness

Your business’s financial health and credit history are vital indicators of your ability to repay the loan. Lenders will scrutinize your business’s profit and loss statements, balance sheets, and tax returns to assess its financial stability. A strong business history, consistent revenue growth, and low outstanding debts will significantly enhance your approval chances.

Personal credit scores also play a role, as they reflect your financial responsibility. Maintaining a high credit score and avoiding excessive debt will boost your chances of loan approval.

Collateral and Loan Terms

Providing collateral, such as real estate or equipment, can increase approval chances and secure favorable loan terms, including lower interest rates. Collateral reduces the lender’s risk by providing an asset that can be seized in case of default. If you have valuable assets that can serve as collateral, don’t hesitate to offer them as part of your loan application.

Additionally, be prepared to negotiate loan terms, such as interest rates, repayment schedules, and covenants. Lenders may be willing to offer more flexible terms to borrowers with strong financial standing and a compelling business plan.

Think of collateral as an insurance policy for the lender. It’s like saying, “Hey, if I can’t repay the loan, you can take this asset instead.” This gives lenders peace of mind and makes them more likely to approve your loan application.

Small Business Loan Approval Rate

Obtaining a small business loan can be a daunting task, with approval rates varying widely. According to a recent study, the overall approval rate for small business loans in the United States is around 25%. However, this number can fluctuate significantly depending on the industry, lender, and borrower’s profile.

Industry Trends

Certain industries are more likely to secure loan approvals than others. Businesses operating in stable and growing industries, such as healthcare, education, and technology, often have higher approval rates. These industries are perceived as having lower risk and higher growth potential, making them more attractive to lenders. Conversely, industries facing challenges, such as retail, hospitality, and construction, may have lower approval rates due to concerns about economic volatility and market saturation.

Lenders’ Criteria

Lenders have different criteria for assessing loan applications, which can impact approval rates. Factors such as the borrower’s credit score, business plan, and financial history play a significant role in determining whether a loan will be approved. Lenders often look for borrowers with strong credit histories, well-developed business plans, and stable financial records. Businesses that can demonstrate a clear path to profitability are more likely to receive loan approval.

Borrower’s Profile

The borrower’s profile can also influence loan approval rates. Businesses with a strong track record of success and a proven ability to repay loans are more likely to be approved. Additionally, businesses that have collateral to secure the loan, such as real estate or equipment, may have a higher chance of approval. Lenders are more comfortable lending to businesses they perceive as low-risk, and a strong borrower profile can help to reduce the perceived risk.

Approval Process

The loan approval process can be lengthy and involve multiple steps. Lenders typically require borrowers to submit a loan application, financial statements, and other supporting documents. The lender will then review the application and make a decision based on the borrower’s profile and the lender’s criteria. If the loan is approved, the borrower will receive a loan agreement outlining the terms of the loan, including the interest rate, repayment schedule, and any other conditions.

Conclusion

Understanding the factors that influence small business loan approval rates can help businesses increase their chances of securing funding. By identifying their industry trends, meeting lenders’ criteria, and improving their borrower profile, businesses can position themselves for loan approval and access the capital they need to grow and succeed.

Small Business Loan Approval Rate: A Detailed Guide for Entrepreneurs

Applying for a small business loan can be a daunting task, but understanding the approval rate and factors that influence it can significantly improve your chances of success. The approval rate for small business loans varies between 20% and 60%, depending on the lender and the specific loan product. In this comprehensive guide, we’ll delve into the intricacies of small business loan approval rates and provide actionable tips to help you boost your approval odds.

Government-Backed Loans

Government-backed loans, such as those offered by the Small Business Administration (SBA), are popular options for small businesses because they offer higher approval rates and more favorable terms. The SBA guarantees a portion of the loan, reducing the risk for lenders and making it more likely that you’ll be approved for the loan. These loans typically have lower interest rates, longer repayment terms, and higher loan amounts compared to traditional loans from banks or online lenders.

Alternative Lenders

Alternative lenders, including online lenders, peer-to-peer lending platforms, and crowdfunding websites, have emerged as viable options for small businesses seeking financing. These lenders often have less stringent requirements and faster approval processes compared to traditional banks. However, they may charge higher interest rates and have shorter loan terms. It’s important to carefully compare the terms and conditions of different alternative lenders before selecting one.

Factors Influencing Approval Rates

Several factors can impact your small business loan approval rate, including your business’s financial health, credit score, industry, and the lender’s underwriting criteria. Lenders will assess your business’s revenue, expenses, profitability, and cash flow to determine its financial viability. Your personal credit score is also a key factor, as it reflects your ability to manage debt. Additionally, the industry in which your business operates can influence your approval rate, as some industries are considered higher risk than others.

How to Increase Your Approval Chances

There are several things you can do to increase your chances of getting approved for a small business loan:

-

Build a strong business plan: A comprehensive business plan outlines your business’s goals, strategies, and financial projections. It demonstrates the viability of your business and its potential for success.

-

Improve your credit score: A higher credit score indicates your creditworthiness and makes it more likely that lenders will approve your loan application.

-

Provide detailed financial statements: Lenders need to see detailed financial statements to assess the financial health of your business. This includes your balance sheet, income statement, and cash flow statement.

-

Get pre-approved for a loan: Pre-approval shows lenders that you’re serious about obtaining a loan and can help you negotiate better terms. It also gives you a better idea of your chances of getting approved for a loan.

-

Explore alternative lending options: If you’re having trouble getting approved for a traditional loan, explore alternative lending options that may have less stringent requirements.

-

Consider a co-signer: If you have a low credit score or limited financial history, getting a co-signer with good credit can improve your chances of getting approved for a loan.

Conclusion

Understanding the small business loan approval rate and the factors that influence it can help you make informed decisions and position your business for success. By building a strong business plan, improving your credit score, and providing detailed financial statements, you can increase your chances of getting approved for a small business loan and accessing the capital you need to grow and thrive.

Leave a Reply