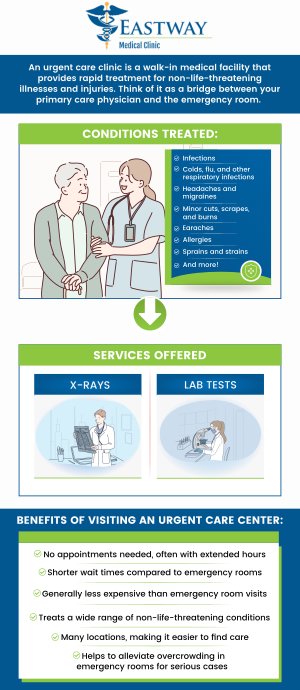

Introduction

Health insurance is a must-have these days. But what if you don’t qualify for traditional health insurance or need extra coverage? That’s where short-term health insurance comes in. Short-term health insurance is a temporary solution that can provide you with peace of mind and financial protection in case of an accident or illness. It’s a great option for people who are between jobs, waiting for their new insurance to kick in, or simply need a little extra coverage.

Short-term health insurance plans are typically less expensive than traditional health insurance plans, and they offer a variety of coverage options to choose from. You can find plans that cover doctor visits, hospital stays, prescription drugs, and more. And, most short-term health insurance plans are renewable, so you can keep your coverage as long as you need it.

If you’re considering short-term health insurance, there are a few things you should keep in mind. First, short-term health insurance plans do not cover pre-existing conditions. So, if you have a pre-existing condition, you will need to find a different type of health insurance. Second, short-term health insurance plans typically have lower coverage limits than traditional health insurance plans. So, if you’re expecting to have major medical expenses, you will need to make sure that your coverage limits are high enough. Finally, short-term health insurance plans can be canceled at any time. So, it’s important to make sure that you understand the terms of your plan before you sign up.

**Short-Term Health Insurance: A Lifeline in Times of Transition**

In life’s ever-changing landscape, we can find ourselves in situations where our health insurance coverage isn’t quite cutting it. Short-term health insurance steps in as a lifeline, offering a flexible and affordable bridge during those gaps. With its quick coverage and tailored options, it’s a smart choice for those transitioning between jobs or facing unexpected medical emergencies.

Advantages of Short-Term Health Insurance

Short-term health insurance boasts a myriad of advantages that make it a valuable option for many. Firstly, it’s incredibly affordable compared to traditional health insurance policies. This makes it an accessible choice for those on a budget or those who only need coverage for a short period of time.

Secondly, short-term health insurance is incredibly flexible. These policies can be tailored to meet your specific needs, whether you require coverage for a few weeks or a year. This flexibility allows you to adjust your coverage as your circumstances change.

Finally, short-term health insurance provides quick and easy access to coverage. Unlike traditional health insurance, which can take weeks to activate, short-term policies can be in effect within a matter of days. This is crucial when faced with unexpected medical emergencies.

**Short-Term Health Insurance: A Lifeline or a Pitfall?**

If you’re between jobs or facing a gap in coverage, short-term health insurance can seem like a lifeline. But, as with any policy, it’s crucial to understand its limitations before you jump in.

**What Is Short-Term Health Insurance?**

Short-term health insurance is a temporary coverage that typically lasts for six months to a year. It’s designed to provide basic medical coverage during short-term transitions, such as job loss or enrollment waiting periods.

**Limitations of Short-Term Health Insurance**

Limited Coverage

Short-term health insurance policies often have significant coverage gaps. They may not cover certain essential health benefits, such as maternity care, mental health services, or prescription drugs. Additionally, they may exclude coverage for pre-existing conditions.

Higher Deductibles

Deductibles are the amount you must pay out of pocket before your insurance starts covering costs. Short-term health insurance policies typically have higher deductibles than traditional health insurance plans. This means you may end up paying more for medical expenses before your insurance kicks in.

Pre-Existing Condition Exclusions

This is a major limitation of short-term health insurance. Many policies exclude coverage for any medical conditions you had before you enrolled. This can be a significant problem if you have a chronic condition, such as diabetes or heart disease.

Eligibility Restrictions

Short-term health insurance may not be available to everyone. Some states have restrictions on eligibility, such as age or health status. Additionally, certain individuals may not qualify for short-term coverage if they have already had a lapse in coverage.

Lack of Guaranteed Renewability

Short-term health insurance policies are not guaranteed renewable. This means that the insurance company can choose not to renew your policy after the initial term expires. This can leave you without coverage if you need it most.

**Before You Enroll**

If you’re considering short-term health insurance, it’s crucial to carefully review the policy. Make sure you understand the coverage limitations, deductibles, and exclusions. It’s also important to consider your health needs and whether short-term coverage is right for you. Remember, it’s often a trade-off between cost and coverage. Weigh the pros and cons carefully before making a decision.

Short-Term Health Insurance: A Safety Net for Your Health

Short-term health insurance is a lifesaver in a health emergency, especially for those who don’t have employer-sponsored coverage. It’s like a safety net, protecting you from the financial burden of unexpected medical expenses. Unlike traditional health insurance that lasts for a year, short-term plans typically cover you for a few months or up to a year, providing flexibility when you need it most.

When to Consider Short-Term Health Insurance

Life is unpredictable, and sometimes our health coverage can be too. Short-term health insurance can come to the rescue when you’re in between jobs, waiting for your employer’s coverage to kick in, or simply need temporary protection during a transition period. It’s also a great option for those who want to avoid the penalties of the Affordable Care Act or simply need supplemental coverage to their current plan.

Benefits of Short-Term Health Insurance

Short-term health insurance offers a range of benefits that make it a smart choice for many people. It’s affordable, flexible, and can provide peace of mind knowing you’re protected in case of an emergency. Unlike traditional health insurance, short-term plans don’t cover pre-existing conditions, but they do provide coverage for accidents, illnesses, and hospitalizations.

Coverage and Exclusions

Short-term health insurance typically covers essential health benefits like doctor visits, prescription drugs, and emergency care. However, it’s important to note that these plans may have higher deductibles and out-of-pocket costs compared to traditional health insurance. Additionally, short-term plans don’t cover routine care like check-ups or preventive screenings. It’s crucial to carefully review the policy details to understand what’s covered and what’s not.

Finding the Right Short-Term Health Insurance

Choosing the right short-term health insurance plan depends on your individual needs and budget. Compare different plans, read reviews, and talk to an insurance agent to find the best option for you. Remember, short-term health insurance is not a long-term solution, but it can provide valuable protection during life’s unexpected twists and turns.

Short-Term Health Insurance: A Lifeline in Healthcare Quandaries

Short-term health insurance has emerged as a valuable lifeline for individuals navigating gaps in coverage. Whether it’s during a job transition, between insurance plans, or for those who don’t qualify for traditional health insurance, short-term policies provide a temporary safety net against unexpected medical expenses.

How to Choose a Short-Term Health Insurance Plan

Selecting the right short-term health insurance plan is crucial to ensure you get the best coverage at an affordable price. Here are some key factors to consider:

1. Understand Your Needs: Start by identifying your specific needs for medical coverage. Are you seeking coverage for routine checkups and minor illnesses, or do you need more comprehensive protection for potential major medical events? Understanding your needs will help you narrow down your search and find a plan that aligns with your priorities.

2. Compare Providers: Explore different providers who offer short-term health insurance. Check their reputation, financial stability, and customer service ratings. Look for providers that have a proven track record of providing reliable coverage and prompt claims processing.

3. Coverage Options: Carefully review the coverage options offered by different plans. These may include coverage for hospitalization, emergency medical services, prescription drugs, and preventive care. Make sure the plan you choose includes the essential coverage types you need.

4. Premium Costs: Premium costs for short-term health insurance vary depending on factors like age, health status, and coverage level. Comparing premium costs from multiple providers will help you find the most affordable option that meets your needs.

5. Duration and Renewability: Short-term health insurance policies typically have a coverage period of up to 364 days. Some providers offer options for renewal, allowing you to extend your coverage if necessary. Consider the duration and renewability options of the plans you’re considering to ensure you have the coverage you need for the desired period.

**Short-Term Health Insurance: A Lifeline in Troubled Waters**

Short-term health insurance can be a life preserver for folks who find themselves treading water without health insurance. But like any insurance, it’s essential to know the ins and outs before jumping in.

**Understanding Short-Term Health Insurance**

Short-term health insurance policies provide temporary coverage for a limited period, typically less than a year. Unlike traditional health insurance, short-term plans offer greater flexibility but come with some key differences. They don’t have to cover essential health benefits like maternity care or prescription drugs, and they may have annual or lifetime limits on coverage.

**Who Benefits from Short-Term Health Insurance?**

Short-term insurance can be a viable option for individuals who:

* Are between jobs and waiting for new coverage to start

* Are self-employed and want affordable coverage

* Are students or recent graduates who need temporary protection

**Shopping for Short-Term Health Insurance**

When shopping for short-term insurance, it’s vital to compare plans and understand the terms and conditions carefully. Consider factors such as the coverage period, premium costs, deductibles, and any exclusions or limitations. Remember, the lowest premium may not always be the best value.

**Limitations of Short-Term Health Insurance**

Short-term health insurance has limitations to keep in mind:

* Limited duration: Coverage typically lasts for less than a year, and renewal is not guaranteed.

* Exclusion of pre-existing conditions: Many plans exclude coverage for pre-existing health conditions.

* High out-of-pocket costs: Deductibles and coinsurance payments can be significant, leading to unexpected expenses.

**Extended Coverage for Short-Term Health Insurance**

In some situations, individuals may be able to extend their short-term health insurance coverage beyond the initial policy period. For example, if they’re waiting for a new job’s health insurance to kick in or encounter unexpected circumstances. However, extensions are typically subject to additional premium payments and may have different coverage terms.

**Additional Tips for Short-Term Health Insurance**

* **Do your research:** Thoroughly explore your options and read reviews before making a decision.

* **Consider your health needs:** Determine the level of coverage you require and choose a plan that meets those needs.

* **Read the policy carefully:** Pay attention to the exclusions, limitations, and renewal terms.

* **Compare quotes:** Obtain quotes from multiple insurers to find the best combination of coverage and cost.

**Conclusion**

Short-term health insurance can offer a temporary lifeline for those without traditional coverage. However, it’s crucial to understand its limitations and carefully evaluate your needs before signing up. By following these tips, you can make an informed decision that provides you with the peace of mind you deserve during life’s unpredictable waters.

Leave a Reply