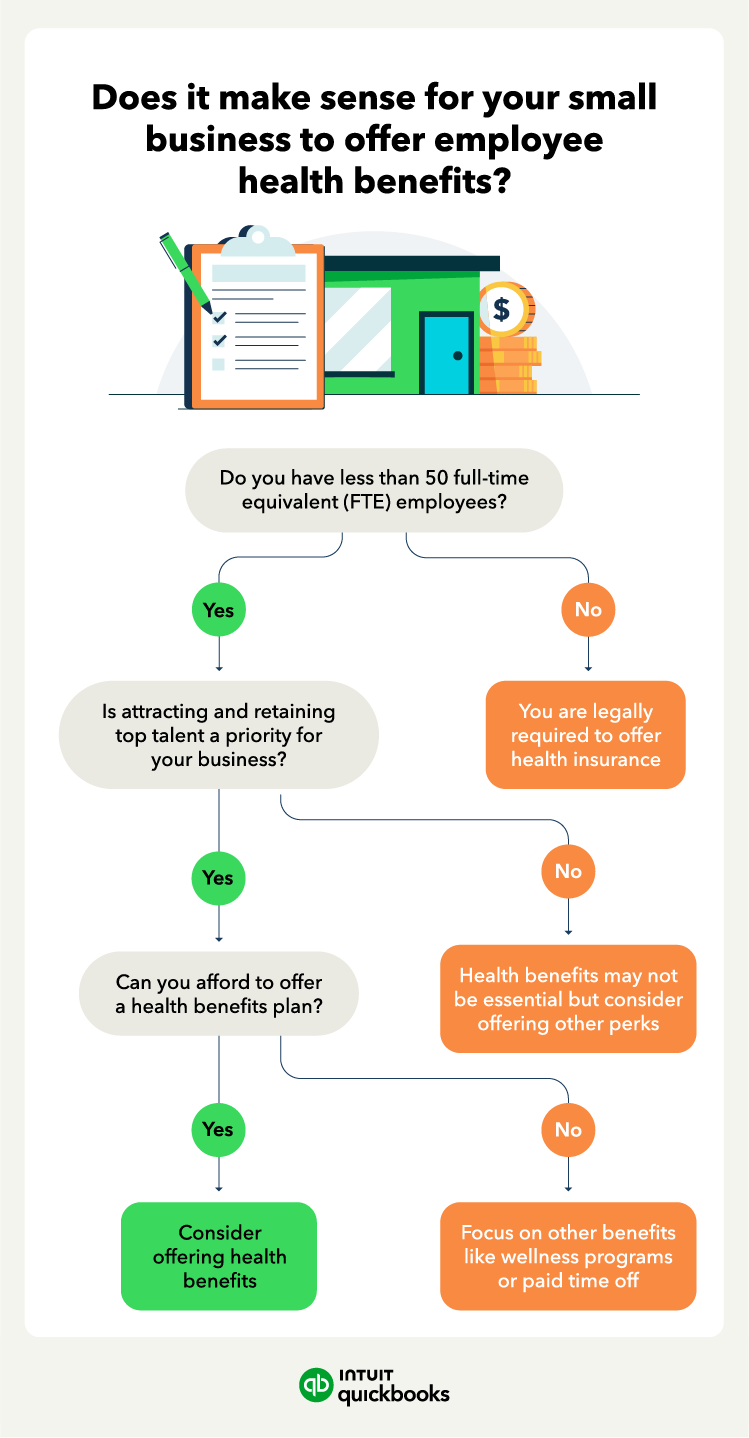

Self-Employed Health Insurance Options: A Complete Guide for 2025

As a self-employed individual, one of the most crucial considerations is finding adequate health insurance coverage. Unlike employees who typically have employer-sponsored health plans, self-employed individuals must navigate the complex world of health insurance on their own. Fortunately, there are several health insurance options available to the self-employed, and understanding them is essential to securing the best coverage for your needs and budget.

Why is Health Insurance Important for the Self-Employed?

Health insurance is vital for everyone, but it holds particular significance for self-employed individuals. Without a company offering health benefits, you’ll need to arrange for your own coverage, ensuring protection from high medical costs and financial instability. Health insurance offers financial security in case of unexpected medical issues or emergencies, and having a comprehensive plan also promotes long-term well-being through preventive care and regular checkups.

However, navigating the maze of options can be overwhelming. The good news is that there are several avenues available to self-employed people, each offering different levels of coverage and flexibility.

1. Health Insurance Through the Marketplace

The Affordable Care Act (ACA) created an accessible online platform where individuals and families can shop for health insurance plans. As a self-employed individual, you can purchase insurance through the ACA marketplace, also known as the Health Insurance Marketplace.

Pros:

- Subsidies and Tax Credits: Depending on your income level, you might qualify for subsidies that lower your premiums or reduce out-of-pocket costs.

- Wide Selection of Plans: You can choose from a range of health insurance plans that cater to different needs, such as Bronze, Silver, Gold, or Platinum plans.

- Guaranteed Coverage: The ACA guarantees that no matter your health condition, you can’t be denied coverage, and there are no annual or lifetime limits.

Cons:

- Limited Enrollment Periods: The marketplace has open enrollment periods, so if you miss the deadline, you might have to wait until the next year unless you qualify for a Special Enrollment Period due to life events like marriage or the birth of a child.

2. COBRA Insurance (Consolidated Omnibus Budget Reconciliation Act)

COBRA is a federal law that allows individuals to continue their employer-sponsored health insurance after leaving their job, provided they worked for a company with 20 or more employees. While COBRA is primarily designed for employees, the self-employed can use it in specific situations. If you were previously employed and had access to an employer-sponsored health plan, you may be able to extend this coverage for up to 18 months under COBRA.

Pros:

- Maintains Existing Coverage: COBRA allows you to keep the same plan you had when employed, ensuring continuity of care.

- No Waiting Period: You don’t have to worry about new waiting periods or exclusions when using COBRA.

Cons:

- Cost: Since you no longer have your employer to share the cost, you’ll be responsible for the entire premium, which can be significantly higher than what you were paying when employed.

3. Private Health Insurance Plans

Private health insurance providers offer a range of plans tailored for self-employed individuals. These plans allow you to choose the exact coverage level you need, from basic catastrophic coverage to more comprehensive plans that include mental health and wellness services.

Pros:

- Customizable Plans: You can choose a plan that fits your specific healthcare needs, whether it’s a low-deductible plan or a high-deductible one paired with a Health Savings Account (HSA).

- Flexibility: Private plans often provide flexibility in terms of coverage options, networks, and benefits.

Cons:

- Higher Premiums: Private insurance plans can be more expensive than those available through the ACA Marketplace, especially if you do not qualify for tax credits or subsidies.

- Limited Coverage in Some Areas: Depending on the insurer and plan, certain regions may have fewer options for medical providers or facilities.

4. Health Savings Account (HSA) with a High-Deductible Health Plan (HDHP)

For self-employed individuals seeking to lower their monthly premiums while still having protection against major medical expenses, pairing a Health Savings Account (HSA) with a High-Deductible Health Plan (HDHP) is a popular option. An HDHP generally offers lower monthly premiums in exchange for higher deductibles.

An HSA allows you to contribute pre-tax dollars to an account, which can be used to pay for qualified medical expenses, including those for your HDHP. The money in an HSA grows tax-free, and the funds roll over year after year.

Pros:

- Tax Benefits: Contributions to an HSA are tax-deductible, and withdrawals for qualified medical expenses are tax-free.

- Lower Premiums: HDHPs have lower monthly premiums than other plans, making them a cost-effective option for self-employed individuals.

Cons:

- High Deductibles: While the monthly premiums are lower, the deductible can be high, meaning you must pay a significant amount out-of-pocket before your insurance kicks in.

- Eligibility Requirements: To qualify for an HSA, you must be enrolled in an HDHP, and there are specific limits on the amount you can contribute each year.

5. Short-Term Health Insurance

Short-term health insurance is a temporary option for individuals who need coverage for a short period, such as during a gap between jobs or while transitioning to a different health insurance plan. These plans are typically less expensive than standard health insurance, but they offer limited coverage.

Pros:

- Lower Cost: Short-term plans usually come with lower premiums compared to long-term health plans.

- Flexible Duration: You can purchase coverage for a few months up to a year, depending on the insurer.

Cons:

- Limited Coverage: Short-term health insurance often doesn’t cover pre-existing conditions, essential health benefits, or preventive care, and may have high out-of-pocket costs.

- Not Available in All States: Short-term health insurance is not available in every state, and some states have restrictions on how long you can stay covered under these plans.

6. Professional Organizations and Associations

Some professional organizations or industry associations offer health insurance plans for their members. These plans are typically designed for individuals in specific fields, such as freelancers, small business owners, or self-employed professionals.

Pros:

- Group Rates: These plans often allow you to access group rates, which can be more affordable than individual insurance plans.

- Tailored Options: Coverage options may be tailored to the needs of your specific profession or industry.

Cons:

- Limited Eligibility: You must be a member of the organization or association to access the insurance, and membership fees may apply.

- Coverage Limitations: Some professional health insurance plans may not offer as much flexibility or variety in coverage as other options.

7. Medicaid and CHIP (Children’s Health Insurance Program)

In some cases, self-employed individuals may qualify for Medicaid or CHIP, especially if their income falls below a certain threshold. Medicaid provides low-cost or free health insurance to individuals and families with low incomes, while CHIP is designed for children.

Pros:

- Low or No Cost: Medicaid and CHIP offer affordable coverage, and in some cases, you may qualify for free or low-cost health services.

- Comprehensive Coverage: Both Medicaid and CHIP provide essential health benefits, including doctor visits, prescriptions, emergency care, and hospital services.

Cons:

- Eligibility Requirements: Your eligibility depends on your income, household size, and other factors. If your income increases, you may no longer qualify.

- Limited Provider Networks: Medicaid and CHIP may have limited networks of doctors and hospitals, which could restrict your access to certain medical services.

8. Spouse or Partner’s Health Insurance

If you’re married or in a domestic partnership, you may be able to join your spouse or partner’s employer-sponsored health plan. This is often an attractive option for self-employed individuals, especially if the spouse has comprehensive health benefits.

Pros:

- Employer-Sponsored Rates: Health insurance through a spouse’s employer may be less expensive than purchasing insurance on your own.

- Comprehensive Coverage: Employer-sponsored plans often offer a wide range of coverage options, including medical, dental, vision, and more.

Cons:

- Eligibility: You must meet certain criteria, and your spouse or partner must work for a company that offers health benefits.

- Limited Control: You won’t have as much control over the plan selection and may be subject to your spouse’s employer’s open enrollment periods.

Conclusion

Finding the right health insurance option as a self-employed individual can seem daunting, but it doesn’t have to be. By exploring the options available, such as the ACA marketplace, private insurance, COBRA, and HSAs, you can find a plan that suits your budget and health care needs. Remember, health insurance is an essential tool for financial protection, ensuring that you have access to quality care when you need it most. Take the time to research your options, compare plans, and choose the best solution for your unique situation.

Leave a Reply