Life Insurance for Smokers: What You Need to Know

Life insurance is a crucial safety net for families, ensuring financial protection in the event of an untimely death. For smokers, obtaining life insurance can present unique challenges, but it’s far from impossible. In this article, we’ll explore how smoking affects life insurance rates, what options smokers have, and how they can increase their chances of securing affordable coverage.

Understanding Life Insurance for Smokers

Life insurance is essentially a contract between an individual and an insurance company, where the policyholder agrees to pay regular premiums in exchange for a lump sum payout to their beneficiaries in the event of their death. This payout can provide financial stability to loved ones, covering funeral costs, outstanding debts, and everyday living expenses.

However, smokers face higher premiums than non-smokers due to the increased health risks associated with smoking. Smoking is a major contributor to many life-threatening health conditions such as lung cancer, heart disease, and chronic respiratory diseases, which can shorten life expectancy. Insurance companies factor in these risks when determining the cost of life insurance for smokers.

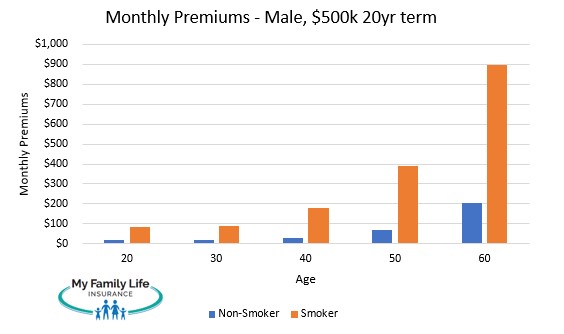

Why Do Smokers Pay Higher Life Insurance Premiums?

Life insurance companies assess risk based on various factors, and smoking is one of the most significant health risks that can affect life expectancy. Smokers are statistically more likely to suffer from serious health conditions, which translates into a higher likelihood of an early death.

Here are some key reasons why life insurance premiums are higher for smokers:

- Increased Risk of Health Problems: Smokers are at higher risk for a wide range of diseases, including lung cancer, heart disease, and chronic obstructive pulmonary disease (COPD). These conditions can significantly reduce life expectancy, making smokers riskier to insure.

- Higher Mortality Rate: Studies show that smokers have a higher mortality rate compared to non-smokers. Insurance companies factor this into their pricing models, leading to higher premiums.

- Long-Term Effects: Smoking doesn’t just affect health in the short term. The long-term impact of smoking, such as chronic diseases that develop over time, adds to the insurance company’s financial risk.

How Smoking Affects Life Insurance Coverage

When applying for life insurance, smokers are typically required to provide a detailed medical history and undergo a medical exam. During the process, an insurance company will assess your risk level, which will influence the premium they offer. Smokers are often classified into different categories depending on the amount of smoking they do.

- Smoker vs. Non-Smoker: Smokers generally pay higher premiums than non-smokers. However, the exact amount depends on how much you smoke and how long you’ve been smoking.

- Heavy vs. Occasional Smoker: Life insurance companies may classify smokers based on how frequently they smoke. Those who smoke more frequently (e.g., a pack a day) will likely face higher premiums than someone who only smokes occasionally.

- Smoking History: Some life insurance policies may consider smokers who have quit for a certain period to be non-smokers, leading to a reduction in premiums. In many cases, a person who has quit smoking for at least 12 months may be eligible for non-smoker rates.

- Medical Underwriting: In some cases, insurance companies may offer policies that do not require a medical exam, such as guaranteed issue life insurance or simplified issue life insurance. These policies tend to have higher premiums, especially for smokers, because the insurer does not have access to detailed health information.

Types of Life Insurance Available for Smokers

While smokers face higher premiums, they still have several options for life insurance coverage. Here are the most common types of policies available to smokers:

- Term Life Insurance: This type of policy provides coverage for a set period, such as 10, 20, or 30 years. It is typically the most affordable option for smokers, as the premiums remain fixed for the duration of the term. However, if you outlive the term, the policy expires, and no payout is made.

- Whole Life Insurance: Whole life insurance provides coverage for your entire life, as long as premiums are paid. While whole life insurance is generally more expensive than term life insurance, it offers the benefit of lifelong coverage and can build cash value over time.

- Universal Life Insurance: Universal life insurance is a flexible policy that combines life coverage with an investment component. The premiums can be adjusted over time, and the policy accumulates cash value. Smokers may face higher premiums for universal life insurance, but it provides flexibility and long-term benefits.

- Guaranteed Issue Life Insurance: This is a type of permanent life insurance that does not require a medical exam or health questions. It is ideal for smokers who may have health issues but still want coverage. However, these policies tend to have higher premiums and lower coverage limits.

- Simplified Issue Life Insurance: Simplified issue policies are similar to guaranteed issue policies but may require some health questions. They are easier to obtain than traditional life insurance policies, but premiums can be higher for smokers.

Tips for Smokers to Get Affordable Life Insurance

While smoking presents challenges when purchasing life insurance, there are several strategies smokers can use to improve their chances of securing more affordable coverage:

- Quit Smoking: The most obvious and effective way to lower life insurance premiums is to quit smoking. Many insurance companies offer non-smoker rates for individuals who have quit smoking for at least 12 months. If you’re serious about quitting, this can significantly reduce your premiums over time.

- Shop Around: Insurance premiums can vary significantly between companies, so it’s important to compare quotes from different insurers. Some companies may offer more favorable rates for smokers, so it’s worth doing your research.

- Consider Term Life Insurance: If you’re looking for more affordable coverage, term life insurance is typically the least expensive option. It provides coverage for a set period, and you can choose the term length that best fits your needs.

- Improve Your Health: Smokers with other health issues, such as obesity or high blood pressure, may face even higher premiums. Improving your overall health can help lower your premiums. Maintaining a healthy weight, exercising regularly, and eating a balanced diet can all contribute to better life insurance rates.

- Consider a No-Medical-Exam Policy: If you have trouble obtaining traditional life insurance due to smoking, consider a no-medical-exam policy. While these policies tend to be more expensive, they can be easier to obtain and may provide a solution for smokers who don’t want to undergo a medical exam.

Conclusion

Life insurance for smokers may come with higher premiums, but it is still possible to find coverage that meets your needs. By understanding the factors that affect life insurance rates for smokers, exploring different policy options, and following strategies to improve your health and lifestyle, you can increase your chances of securing affordable coverage.

While smoking undoubtedly increases the risk of health issues, quitting smoking can have a positive impact on both your health and your life insurance premiums. Be proactive in researching and comparing different life insurance policies to ensure that you and your loved ones are financially protected, no matter your smoking history.

Keywords: life insurance for smokers, smoking and life insurance premiums, smokers insurance rates, affordable life insurance, term life insurance for smokers, quitting smoking and life insurance, best life insurance for smokers, no medical exam life insurance for smokers, life insurance coverage options for smokers, life insurance premiums for smokers

Leave a Reply