Introduction

Searching for the ultimate funding solution to elevate your business to new heights? Look no further than a business loan from banks. These financial lifelines can inject the necessary capital into your entrepreneurial endeavors, whether you’re seeking to launch a groundbreaking startup or expand your existing operations. With a bank loan, you can seize opportunities, overcome challenges, and propel your business towards success.

Eligibility Criteria

Before embarking on the loan application journey, it’s essential to assess your eligibility. Banks typically evaluate various factors to determine your creditworthiness, including your business’s financial performance, credit history, and projected cash flow. A solid track record, positive cash flow, and a well-crafted business plan will increase your chances of securing a favorable loan. Additionally, banks may consider your personal credit score and history, so maintaining a strong financial reputation is crucial.

Loan Terms and Conditions

Dive into the specifics of the loan terms and conditions to ensure they align with your business’s needs. Key considerations include the loan amount, interest rate, repayment period, and any additional fees or charges. Carefully scrutinize these details to avoid any surprises down the road. Remember, the interest rate will significantly impact your monthly payments and the overall cost of borrowing, so compare different loan options to find the best deal.

Application Process

Navigating the loan application process requires meticulous preparation. Assemble a comprehensive loan proposal that includes a detailed business plan, financial statements, and supporting documentation. Clearly articulate your business’s purpose, financial goals, and how the loan will contribute to its success. Banks will thoroughly review your proposal, so take the time to present a compelling and well-organized application. Be prepared to provide additional information or clarifications as requested during the process.

Alternatives to Bank Loans

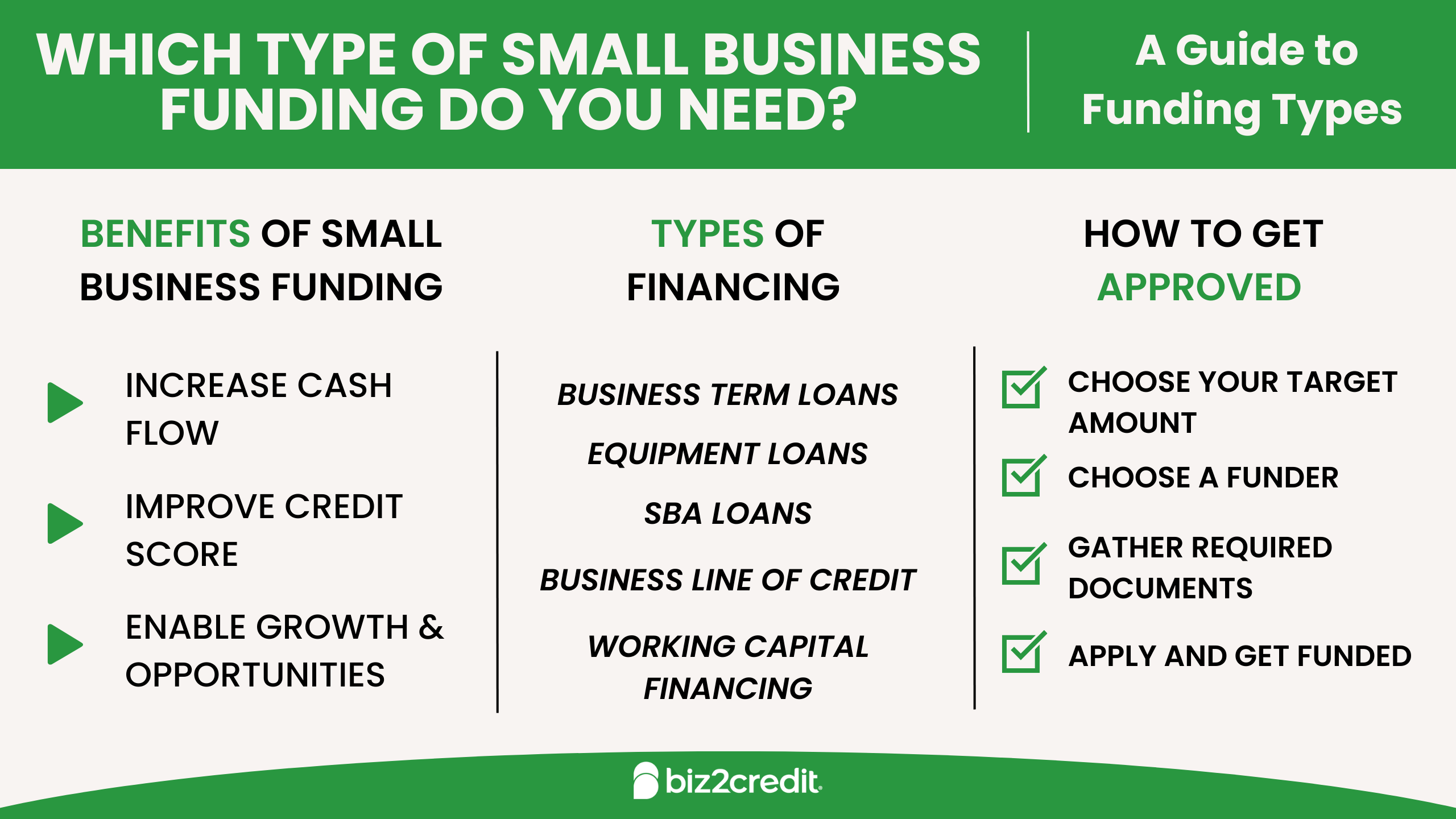

While bank loans are a popular financing option, they may not be suitable for every business. If you face challenges meeting the eligibility criteria or prefer exploring alternative funding sources, consider these options: Small Business Administration (SBA) Loans, Venture Capital, Angel Investments, and Crowdfunding. Each alternative comes with its unique advantages and requirements, so research and evaluate them carefully to determine the best fit for your business.

Business Loans from Banks: A Comprehensive Guide

Getting a business loan from a bank can be a critical step for many entrepreneurs and small business owners. These loans provide the capital needed to start, grow, or expand a business, but they also come with various requirements and processes. To help you navigate the world of business loans from banks, this article will cover key aspects, including eligibility, documentation, and different types of loans available.

Eligibility

Before applying for a business loan, it’s crucial to understand the eligibility criteria set by banks. Generally, businesses must meet certain financial and operational requirements to qualify. One of the most important factors is a strong credit history. Lenders will assess your credit scores to determine your ability to repay the loan on time. Additionally, banks may consider factors such as the business’s age, profitability, and debt-to-income ratio. A viable business plan is also essential, as it outlines your company’s goals, strategies, and financial projections. This plan serves as a roadmap for the bank to evaluate the potential success of your business.

To increase your chances of qualifying for a business loan, you should first check your credit report for any errors or inconsistencies. If necessary, take steps to improve your credit score by paying bills on time and reducing outstanding debt. You should also gather financial documents, such as profit-and-loss statements, balance sheets, and tax returns, to support your loan application. Finally, prepare a comprehensive business plan that clearly outlines your business goals, strategies, and financial projections.

Different Types of Business Loans from Banks

Banks offer different types of business loans to cater to varying business needs. The most common types include:

- **Term Loans:** These are traditional loans with fixed interest rates and repayment periods that range from several months to several years.

- **Lines of Credit:** A line of credit provides access to funds up to a preset limit, allowing businesses to borrow and repay as needed.

- **Equipment Loans:** These loans are specifically designed for businesses to purchase equipment, such as machinery or vehicles.

- **Commercial Real Estate Loans:** These loans help businesses acquire or develop commercial properties, such as office buildings or warehouses.

- **Small Business Administration (SBA) Loans:** Guaranteed by the government, these loans offer more favorable terms and lower interest rates for businesses that meet certain criteria.

When choosing a business loan, consider several factors, including the amount of funding required, the repayment terms, and the interest rate. Each type of loan has its own advantages and disadvantages, so it’s important to carefully assess your needs before making a decision. Consulting with a financial advisor or lender can help you determine the most suitable loan for your business.

Business Loans from Banks: A Guide to Financing Your Business

In the realm of business, securing capital is often a crucial step towards growth and success. Among the various financing options available, business loans from banks stand as a reputable and reliable source of funds. However, before embarking on the journey of obtaining a business loan, it’s essential to delve into the intricacies of loan terms to make an informed decision.

Loan Terms

When it comes to business loans from banks, loan terms play a pivotal role in shaping the overall cost and repayment schedule. These terms typically include the following key elements:

-

Fixed Interest Rate: Many business loans from banks offer fixed interest rates, which provide stability and predictability in interest payments over the loan term.

-

Loan Amount: The amount of money borrowed, which can vary depending on factors such as business needs and creditworthiness.

-

Repayment Period: The duration of the loan, typically ranging from a few years to a decade, over which the borrowed amount and interest must be repaid.

Additionally, other loan terms may include loan fees, collateral requirements, and covenants or restrictions that govern the use of the loan funds. Understanding these terms thoroughly is crucial to ensure that your business can meet the repayment obligations and avoid potential financial pitfalls.

Loan Application Process

To secure a business loan from a bank, you will typically need to go through a loan application process that involves the following steps:

-

Preparation: Gather financial statements, business plans, and other relevant documents to support your loan application.

-

Application Submission: Submit your completed loan application to the bank along with the required supporting documents.

-

Credit Assessment: The bank will evaluate your creditworthiness based on factors such as your personal and business credit history, financial stability, and repayment capacity.

-

Loan Approval: If your application meets the bank’s lending criteria, you will receive a loan approval with specific terms and conditions.

Benefits and Considerations

Business loans from banks offer several benefits, including:

-

Established Credibility: Banks have a long-standing reputation for providing reliable and secure financing options.

-

Access to Larger Loan Amounts: Banks can often provide larger loan amounts compared to other financing sources.

-

Competitive Interest Rates: Banks may offer competitive interest rates, especially for businesses with strong financial performance and credit history.

However, there are also considerations to keep in mind:

-

Loan Approval Process: The loan approval process can be more stringent and time-consuming compared to other financing options.

-

Collateral Requirements: Banks may require collateral, such as real estate or business assets, to secure the loan.

-

Covenants and Restrictions: Loans may come with covenants or restrictions that limit how the loan funds can be used and how the business is operated.

Conclusion

Business loans from banks can be a valuable financing tool for businesses seeking to expand, invest, or overcome financial challenges. By carefully considering the loan terms, application process, and both the benefits and considerations involved, businesses can make an informed decision that aligns with their financial goals and objectives.

Business Loans from Banks: A Comprehensive Guide to Securing Funding for Your Enterprise

For businesses seeking financial support to expand their operations, acquire equipment, or navigate economic downturns, business loans from banks can be a lifeline. However, the application process can be daunting, so understanding the ins and outs is crucial. In this article, we’ll delve into the application process, eligibility requirements, factors affecting approval, and tips for increasing your chances of securing funding.

Application Process

The application process for a business loan from a bank typically involves the following steps:

- Submitting a Loan Application: This document outlines your business’s financial history, future plans, and loan request.

- Providing Financial Statements: Banks require financial statements, such as income statements, balance sheets, and cash flow statements, to assess your business’s financial health.

- Meeting with a Loan Officer: A loan officer will review your application and discuss your loan request. They may ask additional questions and provide guidance on the loan options available to you.

- Underwriting: Once you’ve submitted all necessary documentation, the bank will evaluate your application and make a decision on whether to approve your loan. This process can take several days or weeks.

- Receiving the Loan: If your loan is approved, you’ll receive the loan proceeds in your business account. You’ll then begin making regular payments according to the loan agreement.

Eligibility Requirements

To qualify for a business loan from a bank, your business must typically meet certain eligibility requirements, including:

- Good Credit History: Banks prefer businesses with a solid credit history, demonstrating responsible financial management.

- Strong Financial Performance: Your business should have a history of profitability and positive cash flow.

- Collateral: In some cases, banks may require collateral, such as real estate or equipment, to secure the loan.

- Business Plan: You’ll need to provide a clear and concise business plan outlining your company’s goals, strategies, and financial projections.

Factors Affecting Approval

The bank will consider several factors when evaluating your loan application, including:

- The Purpose of the Loan: The bank will assess how the loan funds will be used and whether they align with the bank’s lending policies.

- The Amount of the Loan: The bank will determine how much they’re willing to lend based on your business’s financial strength and repayment capacity.

- The Interest Rate: Banks will offer different interest rates based on your credit history, the loan amount, and the terms of the loan.

- The Loan Term: The loan term refers to the period over which you’ll repay the loan. Banks typically offer loan terms ranging from a few years to several decades.

Tips for Increasing Your Chances of Loan Approval

To improve your chances of securing a business loan from a bank, consider these tips:

- Build a Strong Credit History: Pay your bills on time and keep your credit balances low to maintain a high credit score.

- Prepare a Comprehensive Business Plan: Outline your business’s goals, strategies, and financial projections to demonstrate your company’s potential.

- Gather Financial Documentation: Gather all necessary financial statements, tax returns, and other documents to support your loan application.

- Explain the Purpose of the Loan Clearly: Specify the intended use of the loan proceeds and how they will benefit your business.

- Consider Collateral: If you have valuable assets, such as real estate or equipment, offer them as collateral to improve your chances of approval.

Securing a business loan from a bank can be a complex process, but with the right preparation, you can increase your chances of success. By following these tips and thoroughly understanding the application process, you can access the funding your business needs to thrive.

Business Loans From Banks

If you’re a business owner in need of financing, one option to consider is a business loan from a bank. Many banks offer a variety of loan products tailored to the specific needs of businesses, and they can be a good source of funding for everything from working capital to expansion projects.

However, it’s important to do your research and understand the terms and conditions of any loan before you apply. Here are some things to keep in mind when considering a business loan from a bank:

Benefits of a Business Loan From a Bank

- Competitive interest rates

- Long repayment terms

- Variety of loan products to choose from

- Convenience of working with a local bank

- Access to other banking services, such as checking and savings accounts

Drawbacks of a Business Loan From a Bank

- Strict eligibility requirements

- Long application process

- Need for collateral or a personal guarantee

- Fees associated with the loan

- Restrictions on how the loan can be used

Documentation

When applying for a business loan, it is important to provide comprehensive documentation to support the application. This documentation will help the bank to assess your business’s financial health and creditworthiness. The following is a list of common documents that you may be required to provide:

- Business plan

- Financial statements

- Tax returns

- Bank statements

- Collateral (if required)

In addition to these basic documents, you may also need to provide additional information, such as:

- Market research

- Sales projections

- Business licenses and permits

- Resumes of key management

- Personal financial statements (if required)

It is important to note that the specific documentation requirements will vary from bank to bank. Be sure to contact the bank that you are considering applying for a loan from to get a complete list of required documentation.

Business Loans from Banks: A Comprehensive Guide

In today’s competitive business landscape, access to capital is crucial for growth and success. Business loans from banks can provide the necessary funding to start, expand, or maintain your operations. This article delves into everything you need to know about securing a business loan from a bank, covering loan approval, types, and more.

Loan Approval

Before you can secure a business loan, you’ll need to navigate the loan approval process. This can take several weeks, and banks typically consider factors such as your business’s creditworthiness, financial statements, and the loan amount. Be prepared to provide detailed information about your business plan, cash flow projections, and collateral.

Types of Business Loans

Banks offer various types of business loans tailored to different needs.

- Term Loans: Repaid over a fixed period, usually in monthly installments.

- Lines of Credit: Provide flexible access to cash up to a predetermined limit.

- Equipment Loans: Financed specifically for purchasing business equipment.

- SBA Loans: Government-backed loans with favorable terms and lower interest rates.

Application Process

To apply for a business loan, you’ll typically need to submit the following:

- Business Plan: Outlining your business objectives, market analysis, and financial projections.

- Financial Statements: Including balance sheet, income statement, and cash flow statement.

- Collateral: Assets pledged to secure the loan, such as real estate or equipment.

Eligibility Requirements

Banks have specific eligibility requirements for business loans. These may vary depending on the bank and loan type, but generally include:

- Time in Business: Most banks require businesses to have been in operation for at least two years.

- Revenue: Banks look for businesses with a certain level of revenue to ensure repayment capacity.

- Credit Score: Business owners with good personal and business credit scores will have a higher chance of approval.

Tips for Success

To increase your chances of securing a business loan, consider the following tips:

- Build a Strong Business Plan: A well-crafted business plan demonstrates your understanding of the market and your ability to succeed.

- Maintain Good Credit: Keep your personal and business credit scores high by paying your bills on time and avoiding unnecessary debt.

- Seek Professional Advice: Consult with a financial advisor or business lender to navigate the loan application process and improve your chances of approval.

Securing a Business Loan from Banks

In the realm of business financing, banks stand tall as formidable pillars, offering a lifeline to entrepreneurs and businesses seeking to expand their ventures. Securing a business loan from a bank involves a meticulous process that demands careful navigation. This comprehensive article will guide you through the intricate steps, empowering you to make informed decisions and maximize your chances of loan approval.

Pre-Approval: Laying the Foundation

Before embarking on the loan application journey, it’s crucial to establish a strong foundation. Gather all the necessary documentation, including financial statements, business plans, and personal credit reports. These documents will serve as the building blocks upon which your loan application will rest.

Loan Application: Presenting Your Case

With your pre-approval papers in hand, it’s time to present your case to the bank. The loan application serves as a roadmap, outlining your business’s financial health, growth prospects, and repayment capabilities. Attention to detail and clarity are paramount, as this document will be scrutinized by loan officers eager to assess your creditworthiness.

Loan Approval: The Green Light

If your loan application passes the rigorous examination process, congratulations are in order! The bank has given its blessing, recognizing the potential in your business. Now comes the moment of signing the loan agreement, a binding contract that spells out the terms and conditions of the loan, including interest rates, repayment schedule, and any collateral requirements.

Loan Closing: Finalizing the Deal

Once the loan is approved, the business will need to sign a loan agreement and provide collateral, if required. Collateral, such as real estate or equipment, serves as a form of security for the bank in the event of default. The loan closing marks the culmination of the loan process. The funds are disbursed, and your business can finally embark on its growth trajectory.

Loan Disbursement: Unleashing the Funds

With the loan closing behind you, the much-anticipated funds are released into your business’s accounts. It’s time to put those carefully crafted plans into action, leveraging the capital to expand your operations, acquire new equipment, or seize new opportunities.

Loan Repayment: Honoring the Commitment

Repaying your business loan on time and in full is not merely an obligation; it’s an investment in your business’s reputation and financial health. Consistent repayments build a strong credit history, making it easier to secure future financing when needed. Remember, a good credit score is like a beacon of trust, attracting lenders and opening doors to new possibilities.

Business Loans from Banks: A Lifeline for Entrepreneurs

Business loans from banks provide a lifeline for entrepreneurs seeking to expand their operations, invest in new equipment, or navigate financial challenges. Banks offer various loan options tailored to the needs of businesses, ranging from short-term loans for quick cash flow to long-term loans for major capital projects.

Loan Eligibility

Before applying for a business loan, it’s crucial to assess your eligibility. Banks typically consider factors such as your credit history, cash flow, collateral, and business plan. Your loan amount and interest rate will depend on these factors, as well as the terms and conditions set by the bank.

Loan Types

There are several types of business loans available, including:

- Short-term loans: These are typically used for immediate financial needs, such as covering payroll or purchasing inventory.

- Long-term loans: These provide larger amounts of funding over extended periods, ranging from years to decades.

- Lines of credit: These allow businesses to borrow funds on an as-needed basis up to a predetermined limit.

- Equipment loans: These specifically finance the purchase of equipment and machinery.

Loan Interest Rates

Interest rates on business loans vary depending on the type of loan, your creditworthiness, and the bank’s prevailing rates. Interest can be fixed (remaining constant throughout the loan term) or variable (fluctuating with market conditions).

Loan Repayment

Loan Repayment

Business loans are typically repaid in monthly installments. The repayment schedule should be carefully managed to avoid default. Failure to make timely payments can damage your credit score and jeopardize your business’s financial stability. It’s important to factor in operating expenses, revenue projections, and other financial obligations when determining your repayment plan.

Loan Collateral

Banks often require collateral to secure business loans, such as real estate, equipment, or inventory. Collateral provides the bank with protection in case of default, as they can seize and sell the assets to recoup their losses.

Loan Application Process

The loan application process typically involves submitting a detailed business plan, financial statements, and personal and business credit information. Banks will thoroughly review your application and may request additional documentation or meetings to assess your eligibility.

Benefits of Business Loans

Business loans offer numerous benefits for entrepreneurs, including:

- Access to capital for growth and expansion

- Improved cash flow and financial stability

- Acquisition of essential equipment and machinery

- Potential tax advantages, as interest payments may be tax-deductible

Business Loans From Banks: A Comprehensive Guide for Entrepreneurs

Business loans from banks can be a lifeline for entrepreneurs looking to start, expand, or maintain their businesses. Banks offer a wide range of loan options, each with its unique terms and requirements. In this article, we’ll explore the ins and outs of business loans from banks, helping you make informed decisions about your financing needs.

Types of Business Loans

Banks offer various types of business loans, including:

- Term loans: A fixed amount of money borrowed for a specific period with regular payments.

- Lines of credit: A flexible loan that allows businesses to draw funds as needed up to a pre-approved limit.

- Equipment loans: Specifically designed to finance the purchase of equipment and machinery.

- Commercial real estate loans: Used to purchase or refinance commercial properties.

- Small business loans: Tailored to meet the financing needs of small businesses.

How to Qualify for a Business Loan

Qualifying for a business loan from a bank requires meeting certain criteria:

- Strong credit history: A good credit score is essential for securing a loan at favorable terms.

- Business plan: A solid business plan outlines your business’s goals, financial projections, and market analysis.

- Financial documents: Banks will review financial statements, tax returns, and other documents to assess your business’s financial health.

- Collateral: Banks may require businesses to provide collateral, such as equipment or real estate, to secure the loan.

- Personal guarantee: In some cases, banks may ask for a personal guarantee from the business owner.

Loan Terms and Conditions

Loan terms and conditions vary depending on the type of loan and the bank you choose:

- Interest rates: Interest rates can be fixed or variable. Fixed rates remain the same throughout the loan term, while variable rates fluctuate.

- Loan terms: Loan terms typically range from a few months to several years.

- Fees: Banks may charge fees for application, origination, and closing costs.

- Prepayment penalties: Some loans carry penalties for paying off the loan early.

Default

If a business defaults on its loan, the bank has several options:

- Repossession: The bank may seize and sell the collateral used to secure the loan.

- Foreclosure: The bank may initiate foreclosure proceedings to sell the commercial property that secures the loan.

- Lawsuit: The bank may file a lawsuit to recover the outstanding balance and any additional costs.

- Negotiation: The bank may be willing to negotiate a payment plan or modify the loan terms to avoid default.

Conclusion

Business loans from banks can be a powerful tool for entrepreneurs. By understanding the different types of loans, qualifying criteria, and loan terms, you can make informed decisions about the financing options available to your business. With careful planning and preparation, you can leverage business loans to fuel your business’s growth and success.

Business Loans From Banks

Business loans from banks can be a valuable source of financing for businesses, but it is important to carefully consider the terms and conditions before applying. Banks typically offer a variety of business loan products, each with its own unique set of features and benefits. It is important to compare the different loan products offered by banks to find the one that best meets the needs of your business.

How to Apply for a Business Loan From a Bank

The process of applying for a business loan from a bank can be complex and time-consuming. However, there are a few steps that you can take to make the process easier. First, you will need to gather all of the necessary documentation, including your business plan, financial statements, and tax returns. Once you have gathered all of the necessary documentation, you will need to complete a loan application. The loan application will ask for information about your business, your financial history, and your plans for the loan proceeds. Once you have completed the loan application, you will need to submit it to the bank for review.

Factors That Banks Consider When Approving Business Loans

Banks will consider a number of factors when approving business loans. These factors include the creditworthiness of the business, the strength of the business plan, and the amount of collateral that the business can offer. Banks will also consider the industry in which the business operates. Some industries are considered to be riskier than others, and banks will charge higher interest rates on loans to businesses in these industries.

Types of Business Loans From Banks

Banks offer a variety of business loan products, each with its own unique set of features and benefits. Some of the most common types of business loans from banks include term loans, lines of credit, and equipment loans. Term loans are repaid over a fixed period of time, while lines of credit can be used to borrow money as needed. Equipment loans are used to finance the purchase of equipment.

Alternatives to Business Loans From Banks

There are a number of alternatives to business loans from banks. These alternatives include venture capital, angel investors, and crowdfunding. Venture capital is a type of investment that is provided to early-stage businesses with high growth potential. Angel investors are individuals who invest in early-stage businesses. Crowdfunding is a way to raise money from a large number of people through online platforms.

Conclusion

Business loans from banks can be a valuable source of financing for businesses, but it is important to carefully consider the terms and conditions before applying. Banks will consider a number of factors when approving business loans, including the creditworthiness of the business, the strength of the business plan, and the amount of collateral that the business can offer. There are a number of alternatives to business loans from banks, including venture capital, angel investors, and crowdfunding.

Leave a Reply