Banks for Business Loans

When it comes to financing your business venture, one of the first places you’ll likely turn to is a bank. Banks have been a mainstay in the lending landscape for centuries, providing businesses with the capital they need to get off the ground, expand their operations, and weather financial storms.

With so many banks out there, each offering a variety of loan products, it can be tough to know where to start your search. That’s why we’ve put together this guide to help you find the best bank for your business loan needs.

What to Look for in a Bank

When choosing a bank for a business loan, there are a few key factors to keep in mind:

- Interest rates: The interest rate you’ll be charged on your loan will have a significant impact on your monthly payments and the overall cost of your loan.

- Loan terms: The loan term, or length of the loan, will determine how long you have to repay the loan.

- Fees: Banks may charge a variety of fees, including origination fees, closing costs, and prepayment penalties.

- Customer service: It’s important to choose a bank that has a good reputation for customer service. You’ll want to be able to reach a customer service representative easily if you have any questions or problems with your loan.

Banks That Offer Business Loans

Here are a few of the banks that offer business loans:

- Wells Fargo

- Bank of America

- Chase

- Citibank

- PNC Bank

Banks for Business Loans

If you’re a business owner, you know that access to capital is essential for growth and success. That’s where a bank loan can come in handy. But with so many different banks and loan products out there, how do you know which one is right for you? Here are a few things to keep in mind when shopping for a business loan.

What to Look for in a Bank Loan

There are a few key factors you’ll want to consider when choosing a business loan, including:

- Interest rates: The interest rate is the amount of money you’ll pay to the bank for borrowing their money. Interest rates can vary depending on a number of factors, including the prime rate, your credit score, and the type of loan you’re getting.

- Fees: In addition to interest, you may also have to pay fees for your loan. These fees can include application fees, origination fees, and closing costs.

- Terms: The term of your loan is the amount of time you have to repay it. Loan terms can vary from a few months to several years.

It’s important to compare all of these factors when choosing a business loan. The best loan for you will depend on your individual needs and circumstances.

What are the Best Banks for Business Loans

Now that you know what to look for in a business loan, let’s take a look at some of the best banks for business loans.

Here are a few of the top banks for business loans:

- Wells Fargo: Wells Fargo is one of the largest banks in the United States, and they offer a variety of business loans, including term loans, lines of credit, and SBA loans.

- Bank of America: Bank of America is another major bank that offers a wide range of business loans. They’re especially known for their small business loans.

- Chase: Chase is another large bank that offers a variety of business loans. They’re known for their competitive interest rates and flexible loan terms.

- U.S. Bank: U.S. Bank is a regional bank that offers a variety of business loans. They’re known for their customer service and their expertise in small business lending.

- Capital One: Capital One is a national bank that offers a variety of business loans. They’re known for their quick and easy loan application process.

These are just a few of the many banks that offer business loans. When choosing a bank, it’s important to compare interest rates, fees, and terms to find the best fit for your business.

Banks for Business Loans

Need a business loan? You’re not alone. Many businesses rely on loans to get started or grow. But with so many banks out there, how do you know which one is right for you? Here are a few things to keep in mind when choosing a bank for a business loan:

–Interest rates: The interest rate is the amount of money you’ll pay to borrow the money. It’s important to compare interest rates from different banks before you decide on one.

–Fees: Banks typically charge fees for business loans. These fees can include application fees, origination fees, and closing fees. Be sure to ask about all of the fees involved before you apply for a loan.

–Loan terms: The loan term is the length of time you have to repay the loan. Loan terms can vary from a few months to several years. Choose a loan term that works for your business’s budget.

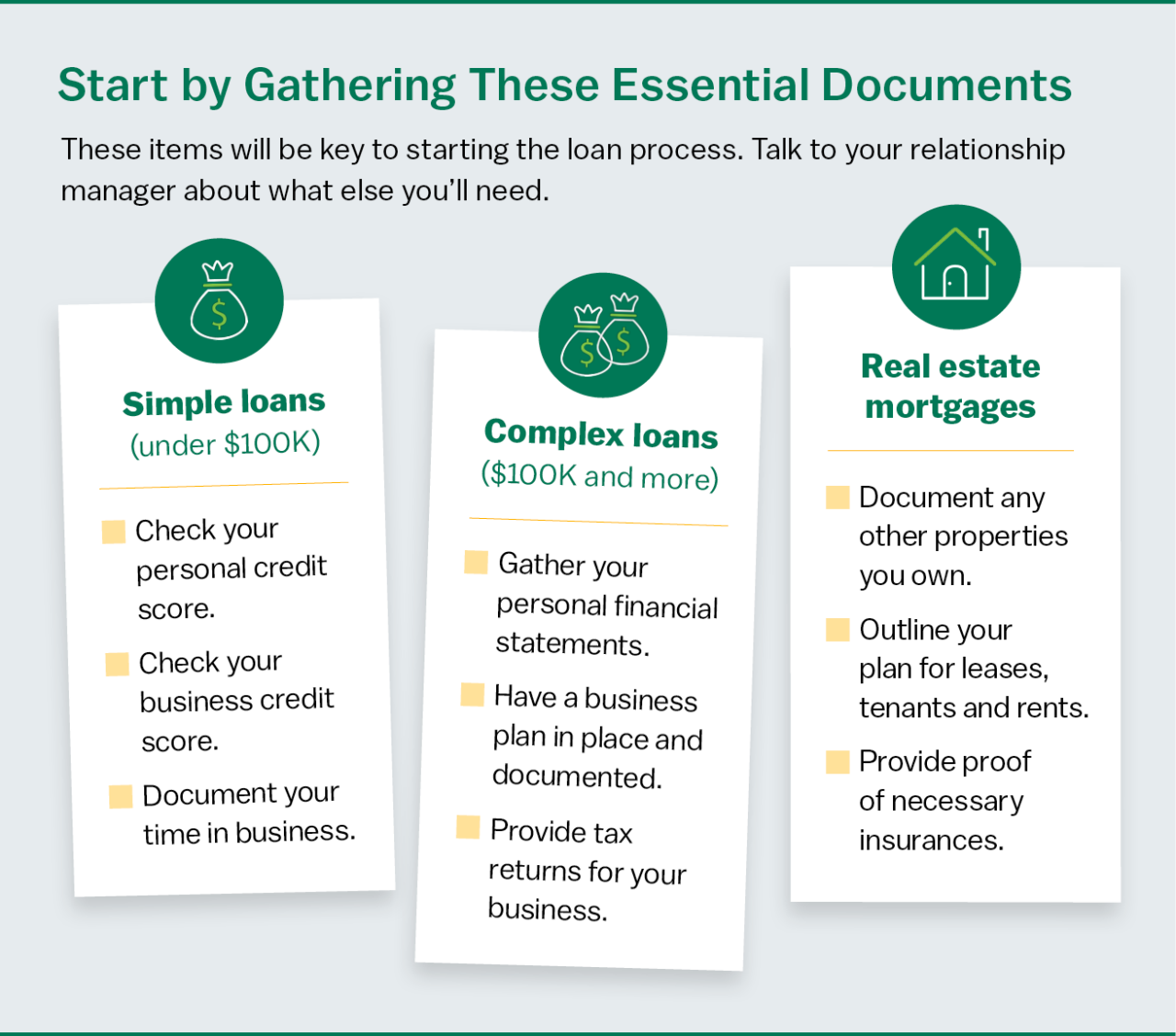

How to Apply for a Bank Loan

The application process for a bank loan typically involves submitting a business plan, financial statements, and other supporting documentation. Here’s a step-by-step guide to applying for a bank loan:

1. Gather your paperwork. The first step is to gather all of the paperwork you’ll need to apply for a loan. This includes your business plan, financial statements, and tax returns. If any of the documents should be signed, make sure to sign them all before submitting them to the bank. You don’t want to get rejected for a loan simply because you forgot to sign a document.

2. Shop around for the best interest rate. Once you have your paperwork in order, it’s time to start shopping around for the best interest rate. Compare interest rates from different banks before you decide on one. A business loan with a higher interest rate might end up costing you a ton of money in the long run.

3. Get pre-approved for a loan. Once you’ve found a bank that you’re interested in, you can apply for a loan. The bank will review your application and decide whether or not to approve you for a loan. Getting pre-approved for a loan can give you peace of mind knowing that the bank is likely to approve you for a loan. This also gives you leverage when negotiating with a landlord or vendor.

4. Close on the loan. Once you’ve been approved for a loan, you’ll need to close on the loan. This involves signing a loan agreement and providing the bank with collateral. Collateral is an asset that the bank can seize if you default on your loan. So, it’s important to choose collateral that you’re comfortable with.

5. Repay your loan. Once you’ve closed on the loan, you’ll need to start repaying the loan. Make sure to make your payments on time each month. Late payments can damage your credit score and make it more difficult to get a loan in the future.

Banks for Business Loans: A Lifeline for Aspiring Entrepreneurs

Accessing capital is the lifeblood of any business venture. For many entrepreneurs, securing a business loan from a traditional bank remains the go-to option. Banks offer a range of loan products tailored to the specific needs of businesses, from startup loans to lines of credit. By partnering with a reputable bank, businesses can tap into a reliable source of funding to fuel their growth and success.

Understanding the Process: Unlocking the Gateway to Funding

Navigating the process of obtaining a business loan can seem daunting, but with proper preparation, businesses can significantly enhance their chances of success. Banks typically require a comprehensive business plan outlining the company’s goals, market analysis, financial projections, and management team. Additionally, they assess the business’s creditworthiness, cash flow, and collateral to determine eligibility and loan terms. By presenting a well-structured application and proactively addressing any potential concerns, businesses can increase the likelihood of securing favorable loan conditions.

Expanding Horizons: Exploring Alternative Financing Options

While banks remain a cornerstone of business financing, alternative sources of funding offer viable options for entrepreneurs seeking non-traditional paths. Venture capital provides equity financing to businesses with high growth potential, offering access to capital and expertise. Angel investors, typically wealthy individuals, invest their own funds in promising startups. Crowdfunding platforms enable businesses to raise capital from a large number of small investors. By embracing these alternative financing avenues, businesses can diversify their funding sources and access capital tailored to their unique circumstances.

Unlocking the Power of Business Loans: Benefits Galore

Business loans offer a multitude of benefits that can empower businesses to thrive. They provide immediate access to capital, enabling businesses to seize opportunities and address urgent needs. By leveraging borrowed funds, businesses can expand their operations, invest in new equipment, or hire additional staff, propelling their growth trajectory. Additionally, business loans can improve cash flow, allowing businesses to manage day-to-day expenses and invest in long-term initiatives.

Tailoring the Fit: Matching Business Loans to Specific Needs

Navigating the diverse landscape of business loans can be akin to searching for the perfect fit in a vast wardrobe. Term loans provide a fixed amount of funding over a specified period, making them ideal for large capital expenditures. Lines of credit, on the other hand, offer flexible access to funds up to a predetermined limit, providing a safety net for businesses facing fluctuating cash flow needs. By aligning the loan type with their specific requirements, businesses can maximize the benefits of financing while minimizing any potential drawbacks.

Leave a Reply