Small Business Insurance: A Lifeline for Thriving Enterprises

In the competitive arena of business, small enterprises face a myriad of risks that can threaten their survival. From unforeseen accidents to costly lawsuits, the path to success is often strewn with potential pitfalls. Small business insurance serves as a safety net, safeguarding your company against financial ruin and protecting your hard-earned assets. This comprehensive guide will delve into the essential aspects of small business insurance, empowering you to make informed decisions that safeguard your business’s future.

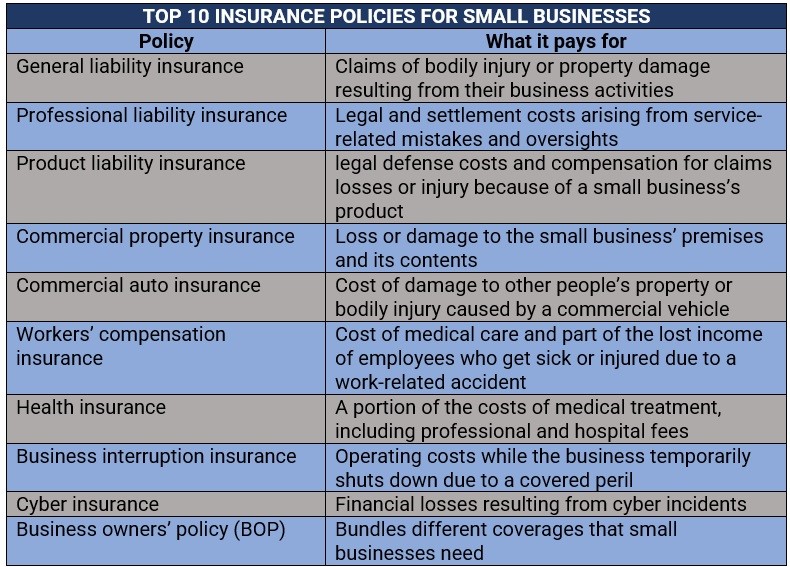

General Liability Insurance: A Shield against Mishaps

Imagine a scenario where a customer slips and falls in your store, sustaining an injury. Or perhaps a faulty product causes property damage to a client’s home. These are just a few examples of the costly claims that can arise from daily business operations. General liability insurance acts as a shield against such financial setbacks, providing coverage for both bodily injury and property damage caused by your business. It’s an indispensable layer of protection for any small business.

Here are some real-life examples of how general liability insurance has saved small businesses from financial disaster:

- A café owner avoided paying out-of-pocket for a customer’s broken leg after they tripped over a loose floorboard.

- A landscaping company was protected from a lawsuit when a falling tree damaged a client’s roof.

- A small retail shop was reimbursed for the costs of replacing a customer’s laptop that was damaged during a repair.

Don’t let unforeseen accidents derail your business’s progress. General liability insurance provides a safety net, ensuring that you can continue operating with peace of mind, knowing that you’re financially protected against the unexpected.

**Small Business Insurance: Your Safety Net When the Unexpected Strikes**

As a small business owner, you’ve poured your heart and soul into your venture. However, even the best-laid plans can go awry, which is where small business insurance comes in. Just like a safety blanket on a cold night, it provides peace of mind and financial protection when the unexpected strikes.

**Business Interruption Insurance: Keeping Your Doors Open Amidst Storms**

Imagine this: a fire devastates your store, forcing you to shut down. The loss of income could cripple your business, but that’s where business interruption insurance steps in. This crucial coverage acts as a financial lifeline by replacing lost revenue and continuing to pay employee wages during the shutdown. It’s like a fire extinguisher for your business, protecting it from going up in flames when disaster strikes.

With business interruption insurance, you can rest assured that your income will still be flowing, even when your business is closed. This buffer allows you to focus on rebuilding and recovering, without the added stress of financial ruin. It’s like having a safety net beneath you, ensuring you won’t fall through the cracks when life throws you a curveball.

**Additional Coverages for Your Business Backpack**

Beyond business interruption insurance, a comprehensive small business insurance policy offers a range of essential coverages tailor-made to address the unique risks you face. These include:

* **Property insurance:** safeguarding your physical assets like buildings, equipment, and inventory.

* **Liability insurance:** protecting you against claims for bodily injury or property damage caused by your business operations, products, or employees.

* **Professional liability insurance:** especially important for service-based businesses, shielding you from claims of negligence or errors in your professional practice.

* **Commercial auto insurance:** covering your business vehicles and providing financial protection in the event of accidents or damage.

Remember, choosing the right small business insurance is not a one-size-fits-all endeavor. The specific coverages you need will depend on the nature of your business, its location, and your individual risk tolerance. By carefully assessing your risks and tailoring your insurance policy accordingly, you can create a safety net that will keep your business afloat through any storm.

Small Business Insurance: A Cornerstone of Protection

In an era where the unexpected can strike at any moment, small business insurance emerges as a lifeline for entrepreneurs. It’s not just a box to check; it’s a shield against unforeseen financial blows that could rattle the very foundation of your business. Whether it’s shielding your assets from lawsuits, compensating injured parties, or covering the costs of a property damage, business insurance provides peace of mind, allowing you to focus on the heart of your enterprise without the gnawing anxiety of potential risks.

Cyber Liability Insurance

In today’s digital landscape, your business is only as safe as your cybersecurity measures. Cyber liability insurance steps into the limelight as your protector against the rising tide of cyber threats. Picture this: a data breach exposes your customers’ sensitive information, and boom, your business could face a barrage of legal repercussions and hefty fines. Cyber liability insurance is your armor, shielding you from the financial consequences of these digital storms, covering expenses such as legal defense, data restoration, and credit monitoring for affected individuals.

Property Insurance

The physical space where your business thrives—whether it’s a buzzing storefront or a cozy office—is not immune to the whims of fate. Property insurance becomes your beacon of hope, standing tall against perils like fire, theft, and natural disasters. It ensures that your business premises and its contents, from your gleaming equipment to your meticulously curated inventory, are financially protected. Think of it as a safety net, providing a financial cushion to help you rebuild or repair your business after an unexpected event.

Errors and Omissions Insurance

Every business, no matter how meticulous, can encounter an occasional misstep or oversight. Errors and omissions insurance, like a trusty umbrella, safeguards you against claims of negligence or mistakes in delivering your services. This coverage extends a helping hand when professional advice or services fall short, protecting you from the financial fallout of these unintentional yet costly errors.

Workers’ Compensation Insurance

Your employees are the lifeblood of your business, and their well-being is paramount. Workers’ compensation insurance steps up to the plate, providing financial assistance to employees who suffer work-related injuries or illnesses. This coverage ensures that your team members receive the medical care and compensation they deserve, safeguarding both their livelihoods and your business’s reputation. It’s not just a legal obligation; it’s a testament to your unwavering commitment to your employees’ well-being.

Small Business Insurance: A Shield Against Financial Calamities

In today’s cutthroat business landscape, safeguarding your venture against unforeseen events is paramount. Small business insurance acts as a robust shield, protecting your livelihood from financial catastrophes. From liability coverage to property insurance, there’s a policy tailored to every business’s unique needs.

Errors and Omissions Insurance (E&O)

E&O insurance is a lifeline for professionals who rely on their expertise to earn a living. Think accountants, lawyers, and consultants. It offers a safety net against claims of negligence or mistakes that result in financial losses for clients.

Negligence, after all, is like a pesky mosquito buzzing around your business. One wrong move, and you could find yourself facing a hefty lawsuit. E&O insurance swat-away those risks, giving you peace of mind to focus on delivering exceptional services without the fear of financial ruin.

Moreover, E&O insurance doesn’t just cover the occasional slip-up. It extends protection to a wide range of errors and omissions. For instance, an accountant who miscalculates taxes, a lawyer who fails to file a document on time, or a consultant who provides faulty advice.

So, if you’re a professional who hangs your hat on your expertise, E&O insurance is your knight in shining armor. It’s a cost-effective investment that can save you a fortune in legal expenses and help you sleep soundly at night.

**Small Business Insurance: Essential Protection for Your Venture**

As a small business owner, you’re wearing many hats and juggling countless responsibilities. One crucial aspect that shouldn’t slip through the cracks is securing comprehensive insurance coverage. Like a safety net, insurance can safeguard your business from unforeseen events that could disrupt its operations or stability.

**Workers’ Compensation Insurance**

Required by law in most states, workers’ compensation insurance is a lifesaver for businesses with employees. It provides wage replacement and medical benefits to workers who suffer injuries or illnesses on the job. This coverage not only protects your employees but also shields your business from costly lawsuits.

**Business Owner’s Policy (BOP)**

A BOP is a tailored insurance package that bundles essential coverages for small businesses. It typically includes property insurance for your building and contents, liability insurance for third-party claims, and business interruption insurance to compensate for lost income if your business is forced to close temporarily.

**General Liability Insurance**

This coverage is like a wide, protective umbrella that protects your business from lawsuits alleging negligence or injuries caused to third parties. It’s crucial for businesses that interact with customers, such as retail stores or contractors.

**Commercial Auto Insurance**

If your business uses vehicles, commercial auto insurance is an absolute must. It provides coverage for accidents, damage, and injuries involving company-owned or leased vehicles.

**Cyber Liability Insurance**

In today’s digital age, protecting your business from cyber threats is more important than ever. Cyber liability insurance can help you cover costs associated with data breaches, ransomware attacks, and other cyber-related incidents.

**Property Insurance**

Property insurance safeguards your business’s physical assets, such as your building, equipment, and inventory. It provides coverage for losses or damage caused by events like fire, theft, or vandalism.

**Health Insurance**

Providing health insurance benefits to your employees is not only a smart investment in their well-being but also a valuable perk that can attract and retain top talent. Group health plans offer a range of options, including medical, dental, and vision coverage.

**Errors and Omissions (E&O) Insurance**

Also known as professional liability insurance, E&O insurance protects businesses that provide professional services. It covers claims alleging negligence or errors in your work that result in financial losses for your clients.

**Directors and Officers (D&O) Insurance**

This coverage is crucial for businesses with a board of directors or executives. It provides protection against lawsuits alleging mismanagement, breaches of fiduciary duty, or other actions that harm the business’s shareholders or stakeholders.

**Umbrella Insurance**

Think of umbrella insurance as an extra layer of protection that kicks in when your other insurance policies run out. It provides additional liability coverage beyond the limits of your underlying policies, ensuring you’re well-covered in the event of a catastrophic loss.

Leave a Reply