Group Business Loans

If you’re a budding entrepreneur looking to launch or expand your enterprise, you may have found yourself exploring financing options. Among the various options available, group business loans, also known as micro-enterprise loans, are specifically tailored to meet the needs of groups of businesses. These loans, often provided by non-traditional lenders such as community development financial institutions (CDFIs), are designed to provide financial support to businesses that may not qualify for conventional bank loans due to limited credit history, lack of collateral, or other factors. With flexible terms and conditions, group business loans empower groups of businesses to access capital and pursue their entrepreneurial aspirations.

Eligibility for Group Business Loans

To qualify for a group business loan, businesses must typically meet certain eligibility criteria. These criteria may vary depending on the lender, but commonly include:

The business must be a for-profit entity, and the loan must be used for business purposes

The business must be located within the lender’s service area

The business must have a clear and viable business plan

The business must demonstrate a need for funding and an ability to repay the loan

The business must be in good standing with all applicable laws and regulations.

In addition to these general requirements, some lenders may have additional criteria, such as minimum time in business or minimum revenue thresholds. It is important for businesses to carefully review the eligibility requirements of potential lenders to determine if they meet the necessary criteria.

Applying for Group Business Loans

The application process for group business loans typically involves submitting a loan application and supporting documentation to the lender. The loan application will typically require information about the business, its owners, and its financial history. Supporting documentation may include financial statements, tax returns, and business plans.

Once the lender has received the loan application and supporting documentation, it will review the materials and make a decision on whether to approve the loan. The lender will consider the business’s eligibility, its financial狀況, and its repayment ability when making its decision.

Repaying Group Business Loans

Group business loans typically have flexible repayment terms, with repayment periods ranging from a few months to several years. The interest rates on group business loans are often higher than those on conventional bank loans, but they are still typically lower than the rates charged by other alternative lenders, such as payday lenders.

Benefits of Group Business Loans

Group business loans offer several benefits to businesses, including:

Affordable financing: Group business loans offer affordable financing options for businesses that may not qualify for conventional bank loans.

Flexible terms: Group business loans have flexible repayment terms, making them a good option for businesses with seasonal or unpredictable cash flow.

Access to capital: Group business loans provide businesses with access to capital that they can use to start or grow their businesses.

Support from lenders: Lenders that offer group business loans often provide technical assistance and other support services to help businesses succeed.

If you’re a business owner looking for financing options, a group business loan may be a good option for you. These loans offer affordable financing, flexible terms, and access to capital, and they can help you start or grow your business.

Group Business Loans: The Lifeline for Small Businesses

In the competitive landscape of today’s business world, small businesses often find themselves strapped for cash. That’s where group business loans come in, offering a lifeline to these ventures. These loans are tailored specifically for small businesses, providing flexible terms and competitive interest rates that big banks might not offer.

Loan Characteristics

Group business loans are typically characterized by their modest size, ranging from $10,000 to $500,000. This makes them an ideal option for businesses that need a quick injection of capital to cover expenses, invest in equipment, or expand their operations. Unlike traditional bank loans, group business loans come with flexible terms, allowing borrowers to choose a repayment period that fits their budget and business needs.

Interest rates on group business loans tend to be competitive, often lower than those offered by banks. This is because group business loans are typically backed by the government or a network of lenders, which reduces the risk for the lender and allows them to offer more favorable rates. As a result, businesses can save money on interest payments, freeing up more funds for their operations.

In addition to their flexible terms and competitive interest rates, group business loans also come with a simplified application process, making it easier for businesses to access the capital they need. Unlike traditional bank loans, which can require extensive paperwork and a lengthy approval process, group business loans can often be approved within a matter of days or weeks.

Group business loans are a valuable resource for small businesses seeking to grow and succeed. They provide access to capital, flexible terms, competitive interest rates, and a simplified application process. If you’re a small business owner in need of funding, consider exploring the option of a group business loan.

Group Business Loans: A Lifeline for Ambitious Entrepreneurs

Group business loans, offered by banks and online lenders, provide a valuable lifeline for entrepreneurs looking to expand their operations or stabilize their financial footing. These loans are extended to businesses that have multiple owners or members, providing them with the capital they need to grow and succeed.

Eligibility Requirements

To qualify for a group business loan, your business must meet specific eligibility criteria. First and foremost, it must be a legally registered entity, such as an LLC or corporation. Secondly, you’ll need a comprehensive business plan that outlines your company’s financial projections, marketing strategies, and growth plans. Finally, you must demonstrate your ability to repay the loan by providing financial statements, tax returns, and other relevant documentation.

Demonstrating Repayment Ability

Lenders are keenly interested in your business’s ability to generate sufficient revenue to cover loan repayments. They’ll assess your financial performance, including your profit margins, sales trends, and overall financial health. To strengthen your application, consider providing additional documents, such as contracts with key clients or projections that demonstrate your business’s earning potential. Remember, lenders are looking for evidence that your business can withstand market fluctuations and generate consistent cash flow.

If you’re concerned about meeting the repayment requirements, explore alternative financing options. These may include microloans, lines of credit, or government-backed loans that offer more flexibility and lower interest rates. By carefully considering your options, you can secure the financing you need to fuel your business’s growth without overextending yourself financially.

Group Business Loans: A Comprehensive Guide for Small Businesses

Are you a small business owner in search of flexible financing options? Group business loans may be the perfect solution. These loans are specifically designed to provide financial support to groups of businesses, offering a range of benefits that can help you grow and succeed.

In this comprehensive guide, we will delve into the ins and outs of group business loans, including the various loan structures, eligibility requirements, and how to apply. We will also provide valuable tips on how to maximize your chances of getting approved and using the loan to its full potential.

Loan Structure

Group business loans are typically structured as revolving lines of credit. This means that you can borrow money as needed, up to a predetermined limit. You will only pay interest on the amount of money you actually borrow. When you repay the loan, the available credit will be replenished, allowing you to borrow again in the future.

Eligibility Requirements

To be eligible for a group business loan, you must meet certain criteria. These criteria may vary depending on the lender, but typically include:

- Strong credit history

- Established business with a proven track record

- Bank statements and financial statements

Application Process

The application process for a group business loan is similar to that of a traditional business loan. You will need to gather the required documentation, complete an application form, and submit it to the lender. The lender will then review your application and make a decision based on your eligibility.

Using Your Loan Wisely

Once you have been approved for a group business loan, it is important to use the funds wisely. These loans can be used for a variety of purposes, including:

- Purchasing equipment

- Expanding inventory

- Hiring additional staff

- Marketing and advertising

By carefully planning how you use the loan, you can maximize its impact on your business.

Conclusion

Group business loans can be a valuable source of financing for small businesses. They offer flexible repayment terms, competitive interest rates, and the ability to access funds as needed. By understanding the loan structure, eligibility requirements, application process, and how to use the loan wisely, you can increase your chances of getting approved and using the loan to its full potential.

Group Business Loans: A Comprehensive Guide for Entrepreneurs

When it comes to financing your entrepreneurial dreams, group business loans can be a lifeline. These loans, extended to a collective of borrowers rather than a single entity, offer several advantages, including reduced risk for lenders and increased access to capital for small businesses. However, like any financial instrument, group business loans come with their own set of drawbacks.

Determining Factors

The eligibility for group business loans typically hinges on the strength of the individual borrowers and the nature of their collective enterprise. Banks and lending institutions assess factors such as personal credit scores, business plans, and collateral to gauge the risk associated with the loan.

Advantages

Group business loans offer numerous benefits, primarily their ability to mitigate risk. By spreading the loan across multiple borrowers, lenders can reduce the potential losses associated with individual borrower defaults. Additionally, these loans often provide access to larger sums of capital than would be available to individual applicants.

Drawbacks

Higher Interest Rates

Group business loans often come with higher interest rates than traditional business loans. This is because lenders perceive the increased risk associated with multiple borrowers. The higher cost of borrowing can significantly impact the overall cost of the loan and should be carefully considered before applying.

Joint Liability

One of the most significant drawbacks of group business loans is the concept of joint liability. In such loans, all borrowers are held equally responsible for the repayment of the debt. This means that if one borrower defaults, the remaining members of the group are obligated to cover the outstanding balance. This can create financial pressure and strain relationships within the group.

Limited Access to Funds

While group business loans can offer larger sums of capital than individual loans, the availability of funds may still be limited compared to traditional financing options. Lenders typically set a maximum loan amount for group loans, which may not be sufficient to meet the needs of larger businesses.

Strict Eligibility Criteria

Qualifying for group business loans can be challenging. Lenders often impose stringent eligibility requirements, including high credit scores, strong business plans, and collateral. This can make it difficult for start-up businesses and entrepreneurs with less-than-perfect credit to obtain financing.

Potential for Conflict

The group dynamics involved in group business loans can sometimes lead to conflict. Differences in financial situations, risk tolerance, and business goals among borrowers can create tensions within the group. These conflicts can hinder decision-making and potentially jeopardize the success of the business venture.

Before considering a group business loan, it’s essential to weigh the potential advantages and drawbacks carefully. By understanding the risks involved and ensuring that the loan aligns with your business goals, you can make an informed decision that supports your entrepreneurial aspirations.

Group Business Loans: A Comprehensive Guide

When it comes to financing their ventures, businesses often encounter a plethora of options, each catering to specific needs. Among these, group business loans stand out as a viable solution for a unique set of circumstances. But what exactly are they, and how do they differ from other financing alternatives? This article delves into the world of group business loans, providing a comprehensive overview of their benefits, eligibility criteria, and potential alternatives.

Group business loans, as the name suggests, involve a collective effort by multiple businesses to secure a loan. These loans are typically offered by non-profit organizations and community development financial institutions (CDFIs). The participating businesses act as a form of mutual guarantee, pledging to repay the loan if one of them defaults. This arrangement often helps businesses that may not qualify for traditional loans due to factors such as lack of collateral or a less-than-stellar credit history.

Eligibility for Group Business Loans

To be eligible for a group business loan, businesses must meet certain criteria. Firstly, they must be independent, for-profit entities operating in the same geographic area. Secondly, they must have a strong business plan and a demonstrated ability to repay the loan. CDFIs and non-profit organizations typically have additional eligibility requirements, such as a commitment to community development or job creation.

Benefits of Group Business Loans

Group business loans offer several advantages to qualifying businesses. They provide access to capital for businesses that may otherwise struggle to obtain financing. Additionally, the mutual guarantee structure reduces the risk to the lender, which often results in lower interest rates and more flexible repayment terms. The collective support of the group can also foster collaboration and knowledge sharing among the participating businesses.

Application Process

Applying for a group business loan involves a thorough process. Interested businesses should contact CDFIs or non-profit organizations that offer such loans. The application process typically includes submitting a business plan, financial statements, and personal guarantees from the principals of each participating business. The lender will then review the application and determine the eligibility and terms of the loan.

Alternatives

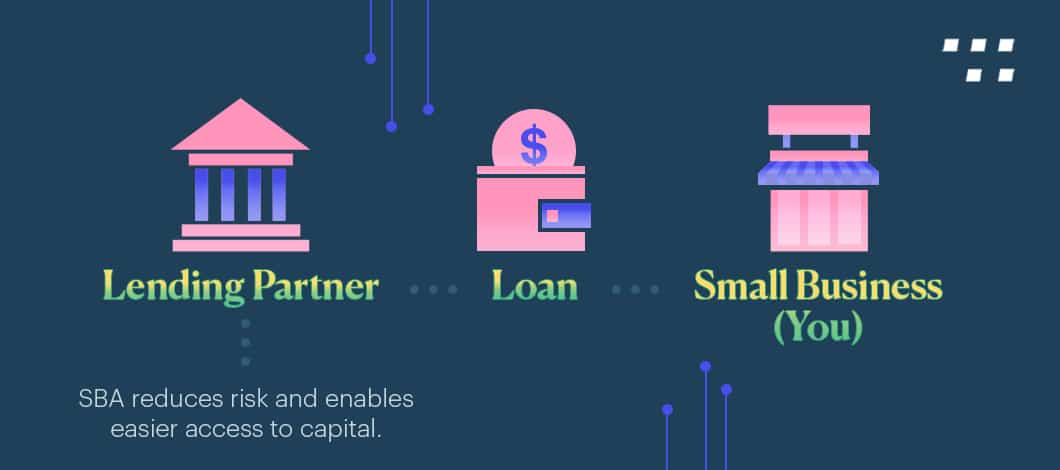

Businesses that do not qualify for group business loans may consider alternative financing options. Traditional business loans, offered by banks and credit unions, require strong collateral and a solid credit history. SBA loans, backed by the Small Business Administration, provide loans to eligible small businesses, often with more favorable terms than traditional loans. Microloans, available through non-profit organizations, are small loans designed for businesses that are just starting out or have limited access to capital.

Conclusion

Group business loans offer a unique and potentially beneficial financing option for businesses that may not qualify for traditional loans. By leveraging the collective strength of multiple businesses, group business loans provide access to capital, reduce risk, and foster collaboration. However, businesses should carefully consider the eligibility criteria and application process to determine if this type of loan is right for them. As always, it’s prudent to explore alternative financing options to find the best solution for their specific needs.

Leave a Reply