Small Business Loans in Florida: A Guide to Navigating Your Options

If you’re a small business owner in Florida, you know firsthand the challenges of starting and growing your business. Access to capital can be a major hurdle, but don’t worry—there are options available to help. One of the most popular is a small business loan. With a little bit of research and planning, you can find the best loan for your needs and get your business off the ground.

Types of Small Business Loans

There are many different types of small business loans available, each with its own unique set of terms and conditions. Some of the most common types include:

- Term loans: These loans are typically used to cover large expenses, such as purchasing equipment or real estate. They are typically repaid over a period of several years.

- Lines of credit: These loans are similar to credit cards, but they are specifically designed for businesses. They can be used to cover short-term expenses, such as inventory or payroll.

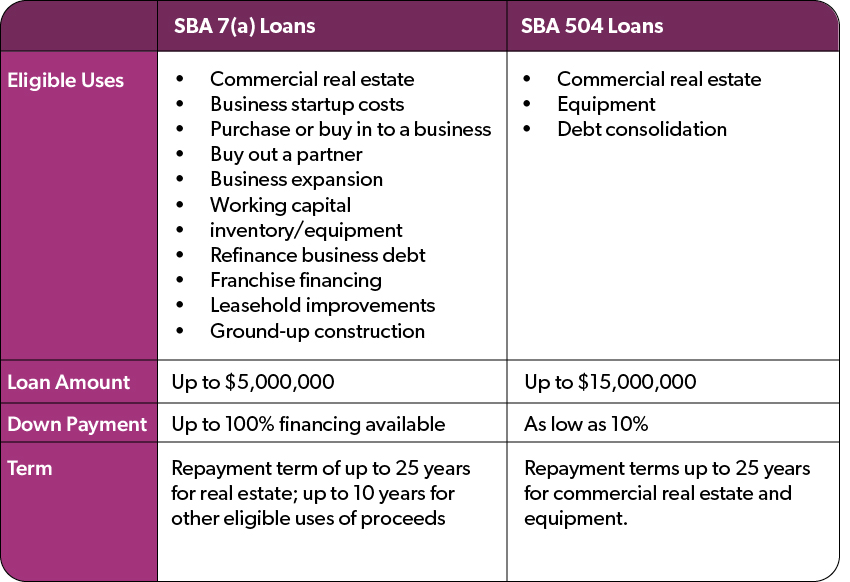

- SBA loans: These loans are backed by the U.S. Small Business Administration. They offer a variety of benefits, such as low interest rates and long repayment terms.

- Microloans: These loans are typically smaller than traditional loans, and they are designed for businesses that do not have access to traditional financing.

How to Apply for a Small Business Loan

The process of applying for a small business loan can be daunting, but it doesn’t have to be. Here are a few tips to help you get started:

- Gather your paperwork: You will need to provide the lender with a variety of documents, such as your financial statements, business plan, and tax returns.

- Shop around: Don’t apply for the first loan you find. Take the time to compare interest rates and terms from multiple lenders.

- Get help: If you need help with the application process, there are a number of resources available, such as the Small Business Administration and SCORE.

Getting Approved for a Small Business Loan

There are a number of factors that lenders will consider when evaluating your loan application, including:

- Your credit score: Your credit score is a measure of your creditworthiness. A higher credit score will improve your chances of getting approved for a loan.

- Your business plan: Your business plan should outline your business goals, strategies, and financial projections. A well-written business plan will show the lender that you have a clear understanding of your business and that you are capable of managing it successfully.

- Your financial statements: Your financial statements will show the lender how your business is performing financially. Lenders will want to see that you are generating enough revenue to repay the loan.

If you have a good credit score, a strong business plan, and solid financial statements, you are more likely to get approved for a small business loan.

How to Get a Small Business Loan in Florida

Florida is a great place to start or grow a small business. The state has a strong economy, a diverse population, and a supportive business environment. If you’re thinking about starting or expanding your business in Florida, you may need to consider a small business loan.

What is a Small Business Loan?

A small business loan is a loan that is specifically designed to help small businesses. These loans can be used for a variety of purposes, such as starting a new business, expanding an existing business, or purchasing equipment. Small business loans are typically unsecured, meaning that they do not require collateral.

How to Qualify for a Small Business Loan

The qualifications for a small business loan vary from lender to lender. However, there are some general requirements that most lenders will look for. These requirements include:

- A strong credit score: Lenders will want to see that you have a good history of repaying your debts.

- A solid business plan: Lenders will want to see that you have a clear plan for how you will use the loan proceeds.

- Sufficient collateral: Lenders will want to see that you have assets that can be used to secure the loan.

- Good cash flow: Lenders will want to see that you have enough cash flow to repay the loan.

How to Apply for a Small Business Loan

The application process for a small business loan is typically straightforward. You will need to submit a loan application to the lender. The application will ask for information about your business, your financial history, and your loan request.

What to Expect After You Apply

Once you have submitted your loan application, the lender will review it and make a decision. The lender will typically notify you of their decision within a few days. If you are approved for a loan, the lender will send you a loan agreement. The loan agreement will outline the terms of the loan, including the interest rate, the loan amount, and the repayment schedule.

Conclusion

If you are considering starting or expanding a small business in Florida, a small business loan may be a good option for you. Small business loans can provide you with the funding you need to get your business off the ground or take it to the next level.

Small Business Loan Florida: How to Secure Funding for Your Venture

Getting a small business loan in Florida can be a major boost for entrepreneurs looking to launch or expand their operations. Here are a few things you can do to increase your chances of getting approved:

- Craft a Compelling Business Plan: Lenders want to see that you’ve done your homework and have a clear vision for your business. Outline your business model, market research, financial projections, and how you plan to use the loan funds.

- Establish a Strong Credit History: Lenders typically check your personal and business credit scores to assess your financial responsibility. Maintain a high credit score by paying bills on time, keeping balances low, and avoiding unnecessary debt.

- Provide Collateral and Personal Guarantees: Offering collateral, such as real estate or equipment, can improve your chances of getting approved. Additionally, personal guarantees, where you pledge your personal assets to repay the loan, can provide additional assurance to lenders.

- Demonstrate Revenue and Profitability: Lenders want to see that your business is generating steady revenue and is profitable. Provide financial statements and tax returns to demonstrate your financial health.

- Research Different Loan Options: Explore various loan programs available in Florida, including loans from banks, credit unions, and government agencies. Compare interest rates, repayment terms, and fees to find the best fit for your business.

- Prepare a Loan Proposal: Put together a comprehensive loan proposal that includes all the necessary information, such as your business plan, financial statements, and collateral. Present it professionally and address any potential concerns the lender may have. This is your chance to showcase your business and convince the lender why they should invest in you. Consider it like pitching your business to a potential investor. Paint a vivid picture of your company’s strengths, growth potential, and how the loan will help you achieve your goals. Anticipate questions and objections, and have well-reasoned responses at the ready. Just like a well-rehearsed sales pitch can increase your chances of closing a deal, a well-prepared loan proposal can vastly improve your odds of securing funding.

Getting a small business loan in Florida doesn’t have to be an uphill battle. By following these tips and presenting your business in the best possible light, you can increase your chances of getting approved and securing the funding you need to grow your venture.

Leave a Reply