Life Insurance Rates To Get You The Best Deal

Getting the best rates can be the difference between peace of mind and financial burden. Our guide will take the mystery out of finding an affordable term life insurance policy that meets your needs.

What is Term Life Insurance?

Imagine term life insurance as a safety net, protecting your loved ones from financial falls after you’re gone. It’s coverage for a set period (often 10, 20, or 30 years) that pays out a fixed death benefit to your beneficiaries when you pass away within that time frame. It’s like a financial parachute, ensuring those who rely on you aren’t left high and dry.

Term life insurance premiums are typically lower than whole life insurance premiums, making it a more budget-friendly option. However, it’s important to keep in mind that term life insurance expires at the end of your policy term. If you want coverage beyond that, you’ll need to renew your policy or purchase a new one.

Think of it as renting an apartment versus buying a house. Term life insurance is like renting – you pay for coverage for a certain amount of time, and when the lease is up, it’s over. Whole life insurance, on the other hand, is like buying a house – you own the coverage for your entire life, but the premiums are typically higher.

The decision between term life insurance and whole life insurance depends on your individual needs and financial situation. If you need affordable coverage for a specific period, term life insurance may be a good option. If you want lifelong coverage and have a higher budget, whole life insurance may be a better choice.

**Best Term Life Insurance Rates: A Comprehensive Exploration**

The search for affordable life insurance policies often leads to the term life insurance option, renowned for its budget-friendly premiums. But navigating the complex landscape of term life insurance rates can be a daunting task. To help you secure the best possible deal, let’s delve into the factors that shape these rates.

**Factors Affecting Term Life Insurance Rates**

When it comes to determining term life insurance rates, insurance companies scrutinize various aspects that can influence the risk associated with insuring you. These include:

**Health Status:**

Undoubtedly, your health status plays a crucial role in determining your premium costs. If you’re in top-notch shape, you’re likely to enjoy lower premiums compared to those with pre-existing health conditions. Insurance companies assess your health through medical exams, reviewing medical records, or simply asking detailed questions about your well-being.

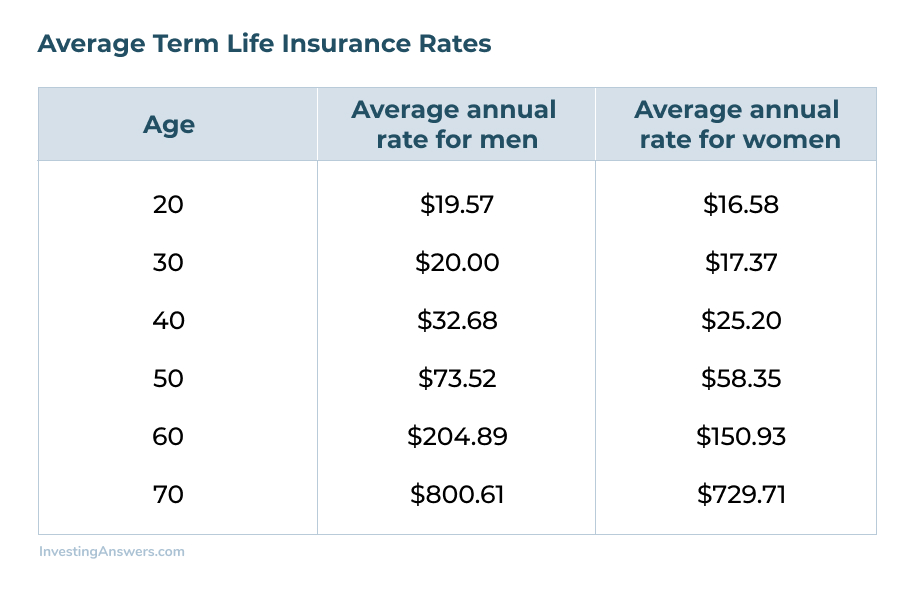

**Age:**

Time takes its toll on us all, and unfortunately, it’s no different when it comes to life insurance rates. The older you are, the higher the premium costs tend to be. This is because, with each passing year, the likelihood of a claim increases. However, securing life insurance while you’re still young and healthy can lock in lower rates for the long haul.

**Lifestyle Habits:**

Your daily habits can have a significant impact on your term life insurance rates. If you engage in risky activities like skydiving or rock climbing, expect to pay higher premiums. Similarly, smoking or excessive drinking can negatively affect your rates. On the flip side, maintaining a healthy lifestyle with regular exercise and avoiding harmful habits can help you secure more favorable terms.

**Coverage Amount:**

The amount of coverage you choose directly influences your premium costs. The higher the coverage, the higher the premiums. It’s essential to carefully consider your financial needs and obligations when determining the right coverage amount. Remember, the goal is to have enough coverage to protect your loved ones without breaking the bank.

**Occupation:**

Your occupation can also play a role in determining your term life insurance rates. If your job involves hazardous activities or frequent travel, you may be quoted higher premiums. It’s important to disclose your occupation accurately to ensure you receive a fair and accurate quote.

**Can You Lock In Low Rates?**

The answer is a resounding yes! By securing term life insurance while you’re young, healthy, and engage in healthy habits, you can lock in lower rates for the duration of your policy. Remember, term life insurance premiums remain fixed for the policy period, so taking advantage of these lower rates can save you a substantial amount of money in the long run.

**Additional Tips for Securing the Best Term Life Insurance Rates**

* **Comparison Shop:** Don’t settle for the first quote you receive. Shop around with multiple insurers to compare rates and find the best deal.

* **Consider Riders:** Riders are optional add-ons that can provide additional coverage, such as for accidental death or dismemberment. While riders can increase your premiums, they may be worth considering for peace of mind.

* **Avoid Overpaying:** Determine your coverage needs accurately to avoid overpaying for unnecessary coverage. On the flip side, don’t skimp on coverage, as it may not be sufficient to protect your loved ones in the event of your untimely demise.

By understanding the factors that shape term life insurance rates and implementing these tips, you can secure the best possible rates and protect your family’s future without putting a strain on your budget.

**

Finding the Best Term Life Insurance Rates

**The search for the most competitive term life insurance rates involves a meticulous examination of various insurance providers and their policies. This exploration should not only consider the financial outlay but also the extent of protection offered. By embarking on a comparative analysis, individuals can optimize their coverage while minimizing their financial burden.

**

Understanding Term Life Insurance

**Term life insurance is a type of life insurance that provides coverage for a predetermined period, typically ranging from 10 to 30 years. Unlike whole life insurance, which offers lifelong protection, term life insurance expires at the end of the specified term. However, it is often more affordable than whole life insurance, making it a viable option for those seeking temporary financial security.

**

Factors Influencing Term Life Insurance Rates

**Several factors play a pivotal role in determining term life insurance rates. These include:

- Age: Premiums increase with age due to the higher risk of mortality.

- Health Status: Individuals with pre-existing medical conditions or risky behaviors may face higher premiums.

- Tobacco Use: Smokers typically pay higher premiums due to the increased risk of health problems.

- Occupation: Certain occupations that involve hazardous activities may lead to higher premiums.

**

Comparing Insurance Providers

**Obtaining the best term life insurance rates requires diligent research and comparisons. It’s crucial to explore multiple providers, seeking quotes that align with specific needs and financial capabilities. Independent insurance agencies can assist in this process, providing unbiased comparisons and guidance.

**

Negotiating the Policy

**Once suitable policies are identified, it’s time to engage in negotiations with the insurance providers. Don’t hesitate to inquire about discounts, such as those offered for healthy lifestyles or multiple policies. Additionally, consider increasing the deductible to lower the premium costs. By skillfully negotiating these terms, individuals can further optimize their coverage without compromising their budget.

Best Term Life Insurance Rates: A Comprehensive Guide to Affordable Coverage

If you’re searching for the most favorable term life insurance rates, you’re in luck. Today’s market offers a myriad of options to help you secure financial protection without breaking the bank. Let’s delve into the ins and outs of finding the best rates that fit your unique needs.

Premium Savvy: Tips for Lowering Premiums

To get the best bang for your buck, consider implementing these premium-saving strategies:

**1. Lifestyle Makeover:** Improving your overall health and lifestyle can lead to lower premiums. Kick bad habits like smoking and excessive drinking, and embrace a healthier diet and exercise routine. Your body and your wallet will thank you.

**2. Non-Smokers’ Advantage:** Maintaining a non-smoking status is a surefire way to reduce your premiums. Insurance companies reward healthy habits, so breathe easy knowing that you’re getting a better deal.

**3. Coverage Countdown:** Choose a shorter coverage period. Just like a shorter car loan has lower monthly payments, a shorter term life insurance policy will have lower premiums.

**4. Face Value Finesse:** Consider policies with lower face values. The amount of coverage you need depends on your individual circumstances. Don’t over-insure yourself; opt for a face value that meets your essential needs to keep premiums in check.

Additional Strategies:

- Compare quotes from multiple insurance providers.

- Check with your employer or professional organizations for group discounts.

- Research no-medical-exam policies for a streamlined application process.

- Consider term life insurance with a return of premium option to get back a portion of your premiums if you outlive the policy term.

**5. Professional Guidance:** Seek personalized advice from an experienced insurance agent. They can assess your specific needs and guide you toward the best term life insurance rates that align with your financial goals.

Best Term Life Insurance Rates

If you’re considering purchasing term life insurance, you’ll want to find the best rates possible. This will help you protect your family financially without breaking the bank. Here are a few tips for finding the best term life insurance rates:

-

Compare quotes from multiple insurers: Don’t just go with the first insurer you find. Take the time to compare quotes from several different insurers to make sure you’re getting the best deal. Many insurance companies now utilize online quoting tools that will allow rates for your specific age, health, coverage amount, and other important factors.

-

Consider your age and health: The younger and healthier you are, the lower your insurance rates will be. Getting started with a policy when you’re young can save you thousands of dollars over the course of your life. If you have any pre-existing health conditions, you may have to pay higher rates.

-

Choose the right coverage amount: The amount of coverage you need will depend on your individual circumstances. Consider your income, debts, and family situation when determining how much coverage you need. You want enough to cover your final expenses and any debts that your family might be responsible for, but you don’t want to overpay for coverage that you don’t need.

-

Shop around for discounts: Many insurers offer discounts for things like being a non-smoker, having a healthy lifestyle, or being a member of certain groups. Ask your insurer about any discounts that you may be eligible for.

Additional Considerations

When evaluating term life insurance options, it’s crucial to assess the financial stability of insurers, consider the possibility of future insurability, and anticipate potential changes in premium rates as the policyholder ages. Here are some additional considerations to keep in mind:

- Financial stability of the insurer: When choosing a term life insurance provider, it’s important to consider the financial stability of the company. You want to be sure that the company will be around to pay out your death benefit when you need it. You can check an insurer’s financial stability by reading their financial statements or by looking at their ratings from independent rating agencies.

- Future insurability: If you’re considering purchasing term life insurance, you should also consider the possibility of future insurability. If you develop a health condition in the future, you may not be able to get life insurance coverage at an affordable rate. That’s why it’s important to purchase coverage while you’re young and healthy.

- Changes in premium rates: Term life insurance premiums are typically level for the duration of the policy. However, some policies may allow for premium increases if the policyholder’s health or lifestyle changes. It’s important to understand how your premium could change over time before you purchase a policy.

By considering these factors, you can make an informed decision about which term life insurance policy is right for you.

Saran Video Seputar : best term life insurance rates

Leave a Reply